AI Is Everywhere. So Where Is the Productivity Boom?

AI adoption is already widespread, but the profits are not. The first phase of the AI trade rewarded companies that built intelligence; the next may reward those that rebuild the enterprise around it.

The Productivity Paradox

AI is now everywhere – except, so far, in most income statements.

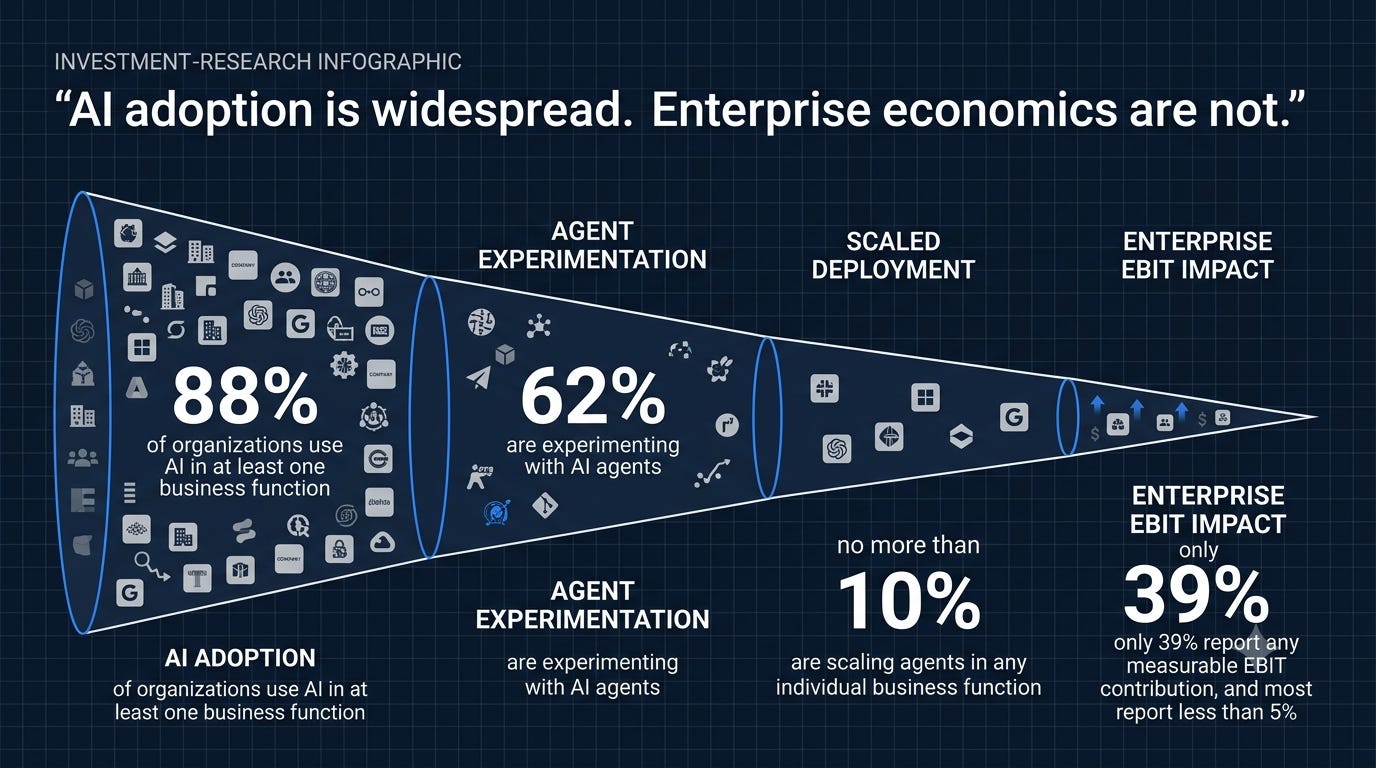

McKinsey’s 2025 survey found that 88% of organizations were using AI in at least one business function, up from 78% a year earlier. Yet only 39% reported any enterprise-level EBIT impact, and most of that group said AI contributed less than 5% of EBIT. Roughly two-thirds had not begun scaling AI across the enterprise. The gap is even clearer with agents: 62% were experimenting, but no more than 10% were scaling agents in any individual business function.

At the same time, Wall Street is underwriting an enormous investment cycle. Goldman Sachs estimates that the largest hyperscalers could spend $754 billion on capital expenditures in 2026 – 83% more than in 2025 – and another $905 billion in 2027. Its equity strategists already assume AI-driven productivity will add 0.4 percentage point to S&P 500 EPS growth in 2026 and 1.5 points in 2027.

Those forecasts may prove right. But they create a burden of proof.

The first three years of the AI trade were driven by scarcity: scarce GPUs, scarce training capacity, and scarce frontier models. The next phase must be driven by returns. Enterprises need enough measurable productivity, revenue growth, or cost savings to justify the infrastructure bill.

Our view is that AI capability is no longer the primary bottleneck.

The bottleneck is organizational.

Most companies are still using AI as a feature: a coding assistant, customer-service bot, meeting summary, or faster search box. These tools can save time at the task level while leaving the surrounding workflow unchanged. Employees still wait for approvals, move data between systems, check permissions, reconcile records, and hand work to another department.

A faster task inside a slow process does not create an enterprise productivity boom.

The data supports this distinction. McKinsey’s AI high performers – about 6% of respondents – were nearly three times more likely than other companies to have fundamentally redesigned workflows. The difference was not simply better models. It was the willingness to change how work moved through the organization.

The Electricity Lesson

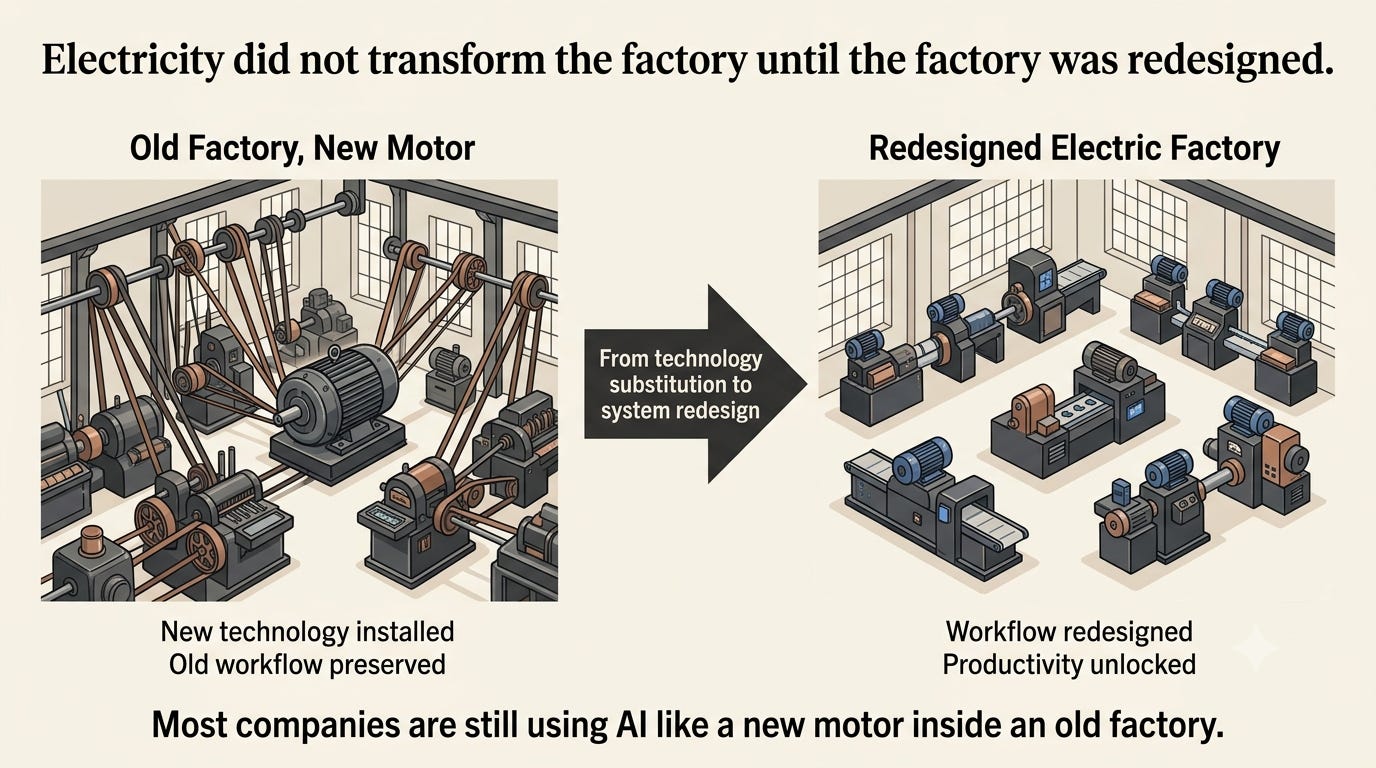

The best historical analogy is not the internet. It is electrification.

Electric motors were commercially available decades before they produced a visible manufacturing productivity boom. NBER research notes that at least half of U.S. manufacturing establishments remained unelectrified until 1919 – roughly 30 years after modern alternating-current systems began spreading.

Early factories treated electricity as a cheaper replacement for steam. They removed the central steam engine, installed a large electric motor, and kept the same line shafts, belts, machine placement, and production sequence.

Energy costs improved, but the factory itself did not.

The larger gains came when managers gave individual machines their own motors. Equipment could be arranged around the flow of materials rather than a central power source. Production could run in smaller units, one breakdown no longer stopped the entire plant, and assembly lines became practical.

Electricity’s killer application was not the electric motor. It was the redesigned factory.

Most enterprises today are attaching an electric motor to a steam-era organization. They are adding copilots to processes built around human handoffs, fragmented databases, functional silos, and management layers designed to coordinate scarce human attention.

AI will not deliver its full value until those processes are rebuilt around machine intelligence:

persistent context, real-time data access, permissioned actions, automated execution, and human review only where judgment is required.

The lesson is not that investors must wait 30 years. Software diffuses faster than industrial machinery. It is that general-purpose technologies require complementary investment – in data, processes, incentives, governance, and organizational design – before their economic value becomes visible.

Where We Are in the AI Cycle

We see three phases.

Phase One: Intelligence Infrastructure

The first phase rewarded companies supplying compute, models, networking, memory, power, and cloud capacity.

$NVDA remains the clearest beneficiary, while $MSFT, $AMZN, $GOOGL, and $META are financing the buildout.

This phase is not over. Goldman expects AI-infrastructure beneficiaries to generate roughly half of total S&P 500 earnings growth in 2026 and 2027. But it is now the consensus trade, and the bar is rising.

The market’s next question is no longer whether hyperscalers can buy more chips.

It is whether customers can earn enough from AI to keep the spending cycle economically rational.

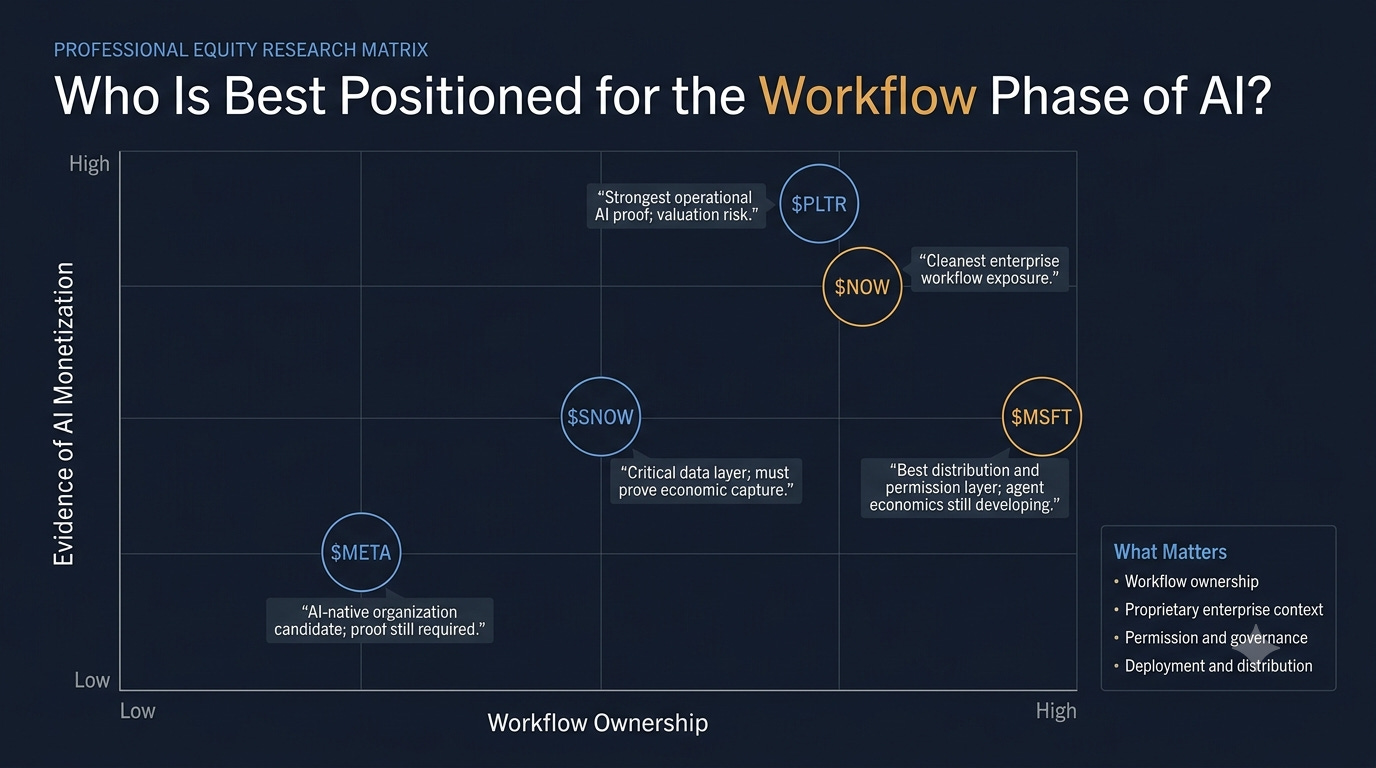

Phase Two: Workflow Reconstruction

This is where we believe the next layer of value creation is beginning.

$MSFT has the strongest distribution advantage.

Paid Microsoft 365 Copilot seats exceeded 20 million in fiscal Q3 2026, while Microsoft 365 commercial cloud revenue grew 19% and paid seats grew only 6%. That gap suggests Copilot is already helping lift revenue per user.

But Microsoft’s longer-term upside depends on moving beyond a premium assistant. It must become the control layer through which agents access documents, applications, identity, and permissions across the enterprise.

That is the difference between selling a useful feature and owning the AI operating layer for knowledge work.

$NOW may have the cleanest workflow ownership.

ServiceNow already sits inside IT, employee, customer-service, security, and approval processes. In Q1 2026, subscription revenue grew 22%, current remaining performance obligations grew 22.5%, and the company signed 16 transactions with more than $5 million of net new annual contract value – nearly 80% more than a year earlier.

Its opportunity is not simply to add AI to existing software. It is to turn existing workflows into agent-executed workflows.

The risk is execution: acquisition spending and platform expansion could pressure margins before incremental AI monetization becomes visible. For investors, the key test is whether AI produces stronger contract growth and operating leverage – not merely higher product-development spending.

$PLTR provides the strongest current evidence that enterprises will pay for operational AI rather than generic copilots.

In Q1 2026, total revenue grew 85%, U.S. commercial revenue grew 133%, and adjusted operating margin reached 60%.

AIP connects models to enterprise data, permissions, decisions, and real-world actions. That is much closer to factory redesign than task assistance.

The investment problem is valuation. Palantir may be the clearest proof of the thesis while also pricing in years of exceptional execution. A strong business thesis does not automatically mean an attractive entry price.

$SNOW owns a critical input: enterprise data context.

Fiscal Q1 2027 product revenue grew 34%, remaining performance obligations reached $9.21 billion, and net revenue retention was 126%.

But data ownership does not guarantee workflow ownership. Snowflake must prove that Cortex and its broader AI stack can turn stored data into governed, production-level actions without becoming a commoditized infrastructure layer.

For $SNOW, the bull case is that enterprise AI increases the value of governed, centralized data. The bear case is that the model and application layers capture most of the economics while data platforms compete on price and compute efficiency.

Phase Three: The AI-Native Organization

In the third phase, companies will redesign headcount, management layers, product development, customer service, pricing, and capital allocation around AI.

$META is one plausible candidate. Its vertically integrated consumer platforms, proprietary data, direct distribution, and founder-led governance give it greater freedom than many incumbents to change how the organization operates.

But investors should not declare Meta “the new Ford” based on management rhetoric or a large AI budget.

The evidence should be measurable: sustained gains in revenue per employee, faster product cycles, lower operating friction, and stronger margins after accounting for AI capex.

The first phase of the AI trade was about building intelligence.

The second is about embedding it into work.

The third will be about rebuilding the company itself.

That is where the productivity boom – and the next set of equity winners – should finally become visible.

Go deeper -

For overnight insight, check the Morning Insights posts.

For intraday developments, follow our Midday posts.

For the close, the wrap, and next-day trade ideas, read the Evening Memo.

For deeper work, Forward Valuation covers multi-week single-name setups (paid subscribers only).

Deep Dive is where we publish our full thematic research for paid subscribers.

Informational only; not investment advice. Sources deemed reliable.