By the Time Wall Street Wraps a Theme in an ETF, You Are Probably Late

When a theme gets its own ticker, the market is usually no longer discovering it. It is distributing it. The real question is whether you spotted the theme before Wall Street packaged it.

A new ETF launches around a hot theme, and the natural reaction is to think the opportunity has arrived. In reality, that moment often means the opposite: the story is no longer early, no longer niche, and no longer under-owned. It is finally easy enough to sell.

Hot Launch, Familiar Pattern

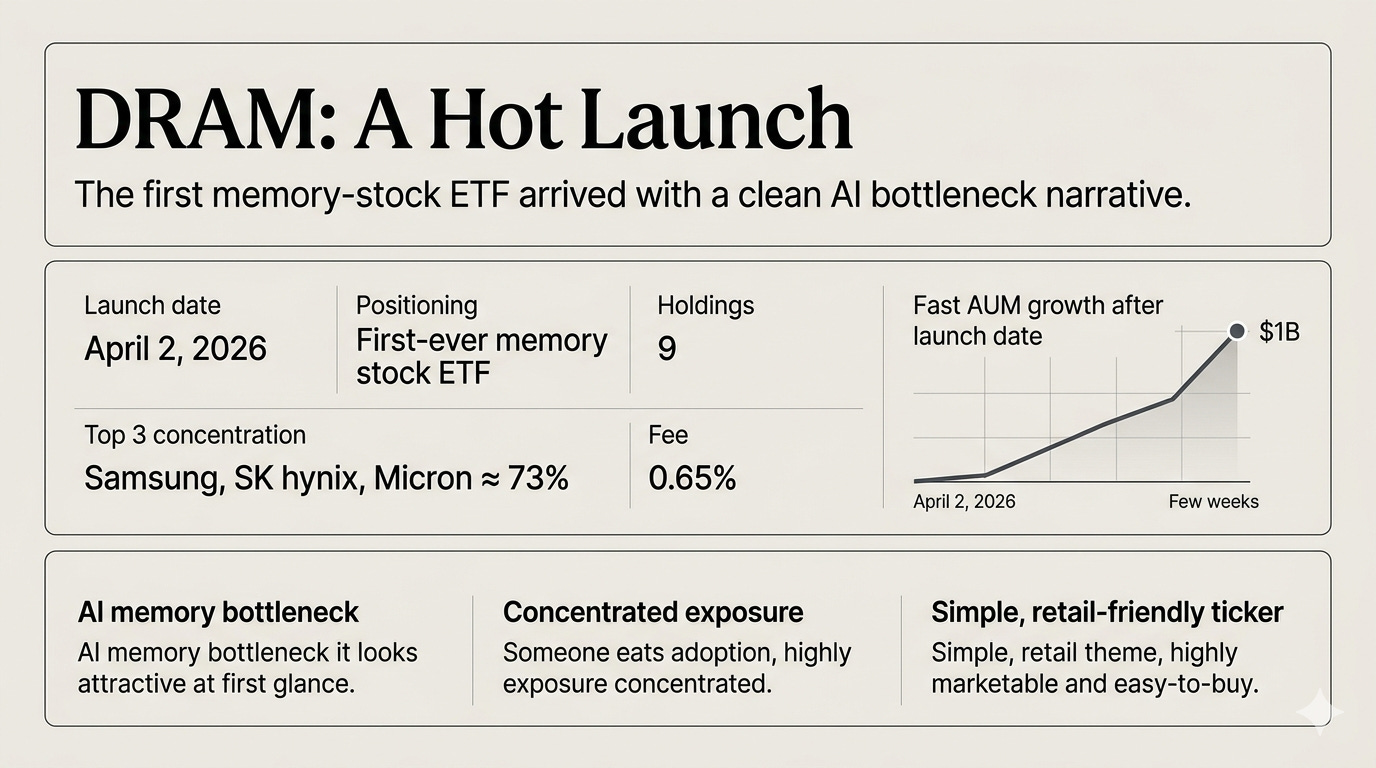

DRAM is exactly the kind of product that feels impossible to ignore. It began trading on April 2, 2026 as the first-ever memory stock ETF, wrapped in one of the cleanest narratives in the market: memory as the bottleneck of the AI buildout. The pitch is neat, intuitive, and easy to repeat. If AI infrastructure keeps scaling, then HBM, DRAM, and storage should matter more, not less. Roundhill packaged that idea into a single ticker with just nine holdings, and more than 73% of the fund sits in three names alone: Samsung, SK hynix, and Micron. The fee is 0.65%, and this is not broad semiconductor exposure. It is a concentrated, highly marketable theme trade.

And the market response has been explosive. DRAM crossed $1 billion in assets just two weeks after launch, one of the fastest ETF debuts of the year. That kind of speed tells you something important: this was not a theme waiting to be discovered. It was a theme waiting to be packaged.

That is exactly where the contrarian instinct should kick in. When Wall Street can turn a story into a clean ticker, a tight basket, and a retail-friendly pitch, investors should at least consider the possibility that the “easy” part of the trade is already behind them. Morningstar has made the same point more bluntly: by the time investors hear about a theme and there are funds ready to track it, much of the growth may already be priced into the underlying stocks.

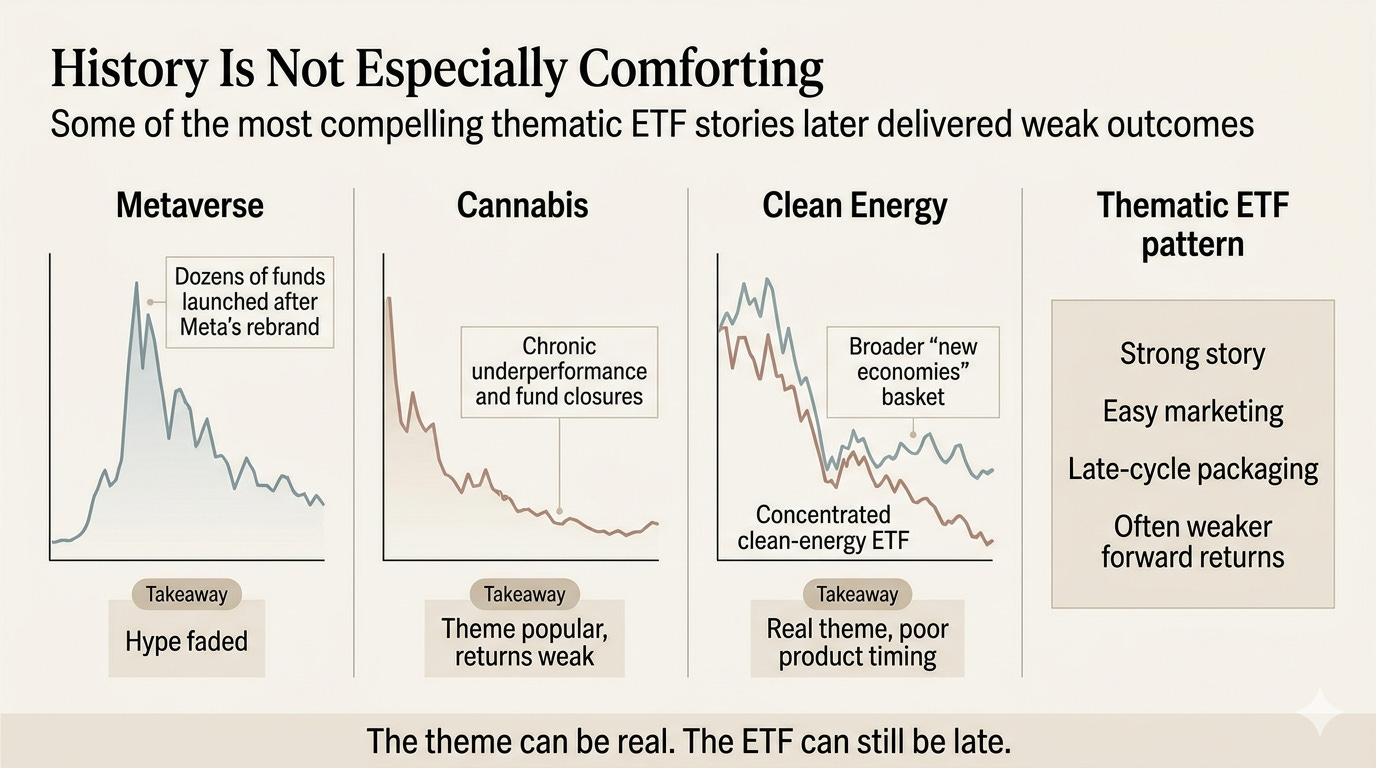

History is not especially comforting. The metaverse boom produced dozens of funds after Meta’s rebrand, only for weak adoption and poor asset gathering to expose how quickly the product machine can outrun real demand. Cannabis was worse: Morningstar data cited by the Financial Times showed cannabis ETFs underperformed the broader market by 39% a year over the past five years, with 13 closures since 2023. Even clean energy offered the same lesson. Over the two years before late 2025, the concentrated Invesco WilderHill Clean Energy ETF fell 39.6%, while a broader “new economies” basket gained 25.7%. The theme can be real. The ETF can still be late.

History is not especially comforting. The metaverse boom produced dozens of funds after Meta’s rebrand, only for weak adoption and poor asset gathering to expose how quickly the product machine can outrun real demand. Cannabis was worse: Morningstar data cited by the Financial Times showed cannabis ETFs underperformed the broader market by 39% a year over the past five years, with 13 closures since 2023. Even clean energy offered the same lesson. Over the two years before late 2025, the concentrated Invesco WilderHill Clean Energy ETF fell 39.6%, while a broader “new economies” basket gained 25.7%. The theme can be real. The ETF can still be late.

When the Story Gets Packaged, Future Returns Often Get Worse

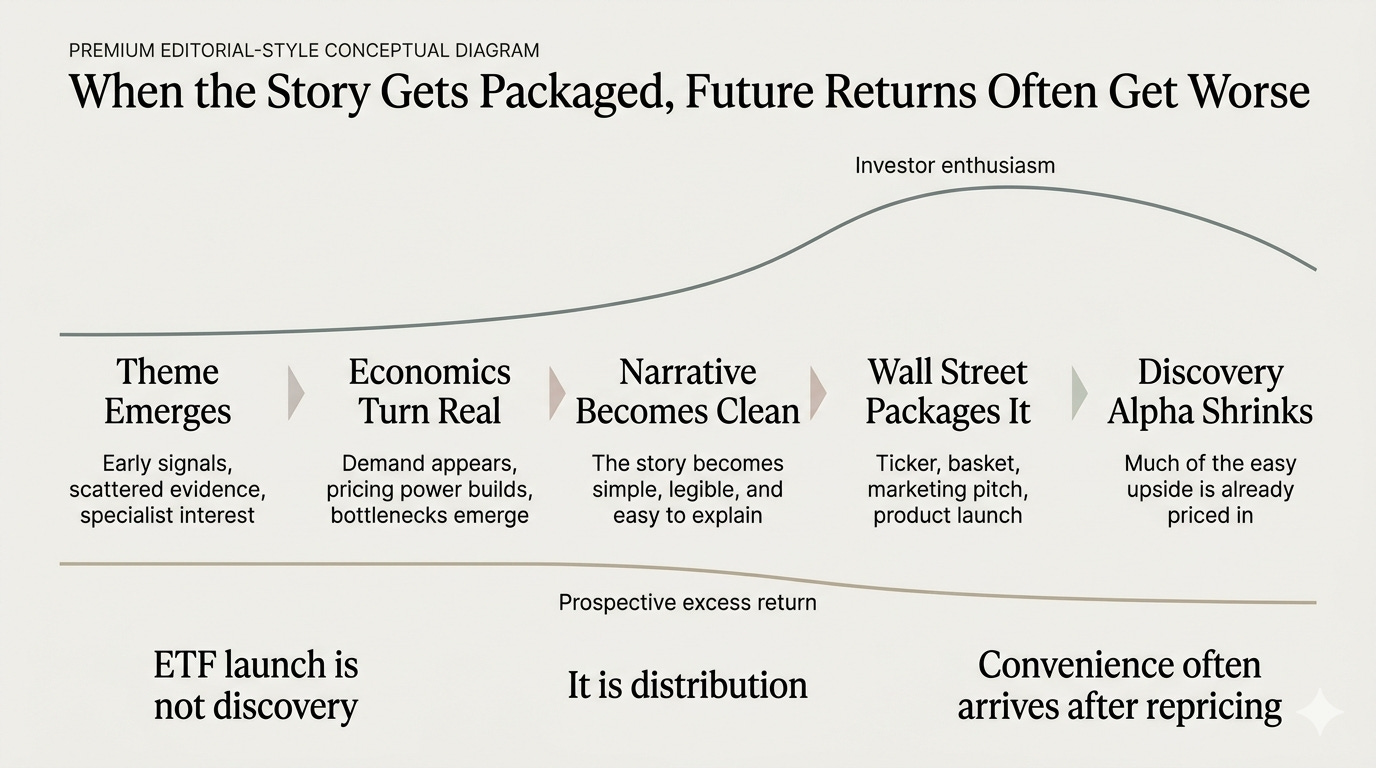

That is the real point. A thematic ETF usually does not appear when a market is still discovering an idea. It appears when the idea has already become legible, repeatable, and commercially useful. By the time an issuer can turn a theme into a clean ticker, a simple pitch, and a retail-friendly basket, the market has often already done the hardest part of the repricing. The ETF is not the birth of the story. It is the distribution of the story.

Morningstar’s work on thematic funds points to the same pattern from the industry side. Asset managers tend to launch these products after trends have already taken hold, often late in bull markets, because that is when a differentiated product is easiest to sell. The funds are narrow, concentrated expressions of a single narrative, often wrapped in a higher-fee structure. Morningstar’s framework is revealing: investors need a real theme, the right beneficiaries, and a market that has not already priced in most of the upside. That third condition is the one investors most often miss.

The academic version of this argument is even harsher. In an NBER working paper on specialized U.S. equity ETFs, the authors argue that these products increasingly cater to demand for popular, attention-grabbing, and already overvalued themes and sectors. Their central finding is not just that specialized ETFs disappoint on average. It is that the underperformance is concentrated in the early years after launch, exactly when enthusiasm is highest. Newly launched specialized ETFs underperform by about 6% a year on a four-factor alpha basis in their first five years, and over that same window they lose roughly 30% in cumulative risk-adjusted terms. The paper’s interpretation is blunt: by the time the ETF enters the market, the underlying securities have often already reached a valuation peak, and the product ends up serving investors who are extrapolating yesterday’s returns into tomorrow.

That does not mean every thematic ETF is doomed, or that every hot theme is fake. It means the burden of proof changes once the theme becomes a product. At that point, investors are no longer being paid for noticing something early. They are being asked to pay for convenient access to something the market already understands. And that is exactly why the right question is not “Should I buy the ETF?” The right question is: what did this theme look like before Wall Street made it easy to buy?

The Better Entry Comes Earlier

If thematic ETFs tend to arrive late, then the practical question is not whether you are early or late in calendar time. It is whether you are early or late in narrative maturity. The worst time to buy is often when a story is finally clean enough to package. The better time is usually earlier: after the economics have started to turn real, but before Wall Street has standardized the trade and distributed it in a ticker.

A useful way to think about that window is through three tests: Proof, Breadth, and