From Narrative to Math: The Thin Cushion Under U.S. Stocks

Four valuation signals are stretched, and the next leg hinges on yields and earnings revisions – not narrative.

Why This Conversation Matters Now

Markets are still priced like the cycle is friendly, but the tape is telling you the cushion is thinner. U.S. equities are hovering close to recent highs, yet intraday moves have gotten choppier as investors juggle two competing narratives: a cooling-inflation / easing-path story on one side, and “AI spending expectations are too perfect” plus softer pockets of demand on the other. On Feb 20, 2026, the S&P 500 finished up just 0.69% at 6,909.51 after swinging between a solid gain and a meaningful intraday drawdown – an unusually noisy day for an index sitting near the top of its range.

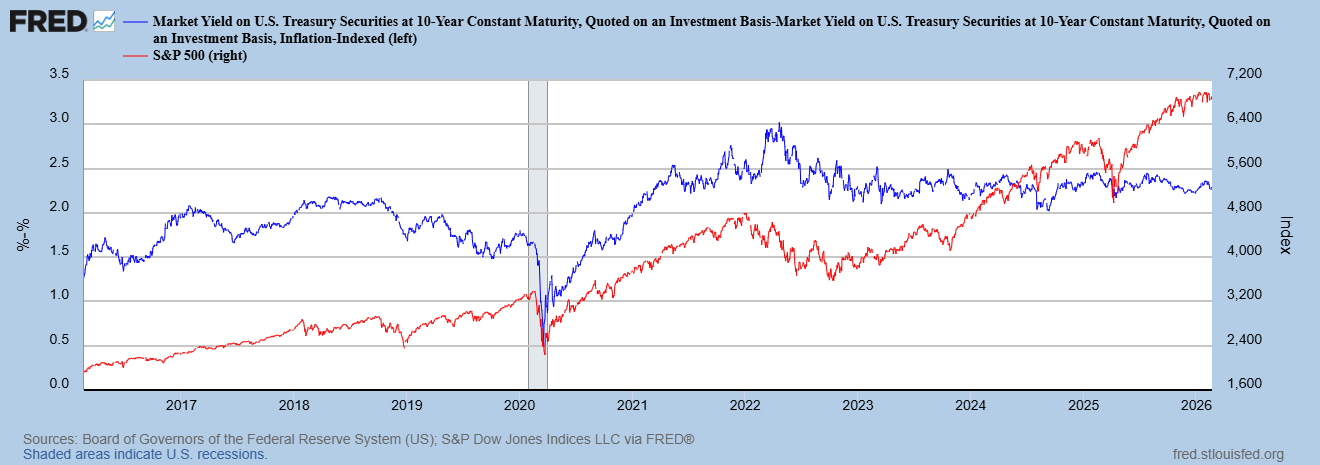

At the same time, the bond market is sending a clear message: yields are drifting toward the low-4% area, but they are not “low.” The 10-year Treasury yield was around 4.05% on Feb 17, after recently testing roughly 4.01% intraday – near early-2026 lows. Real yields are also meaningfully positive (10-year TIPS real yield around ~1.80% on the latest available reading), reinforcing that the discount-rate backdrop is fundamentally different from the 2010s.

That’s why this is the right moment to talk about valuation pressure. When the risk-free rate is ~4% and real yields are positive, multiples become structurally more fragile: the market can’t lean on “rate gravity” to justify paying ever higher prices for future earnings. In this regime, equities can still go up – but the engine changes: returns have to be earned through earnings delivery and breadth, not granted through multiple expansion.

The 10-year Treasury yield finished at around 4.04%. Real yields were also elevated: the 10-year TIPS constant-maturity series printed ~1.80% on the latest available trading day (Feb 12, 2026).

What the market is implicitly pricing. At today’s valuation levels, there are only a few consistent ways math works:

Either rates fall meaningfully (lower discount rate supports higher P/E),

or earnings delivery stays strong enough to “grow into” the multiple,

otherwise the balance of risks shifts toward multiple compression (paying less per dollar of forward earnings).

This is the core point: with a higher discount rate regime, equity upside is more earnings-led than multiple-led, and the market’s tolerance for disappointments is lower. That does not guarantee an immediate drawdown; it means the valuation buffer is thinner and the path becomes more sensitive to rates and revisions.

The Evidence Stack: Four Signals of a Thin Cushion

To argue “valuation pressure is extreme,” you want independent measures that point the same way – different lenses, same conclusion. Here are four:

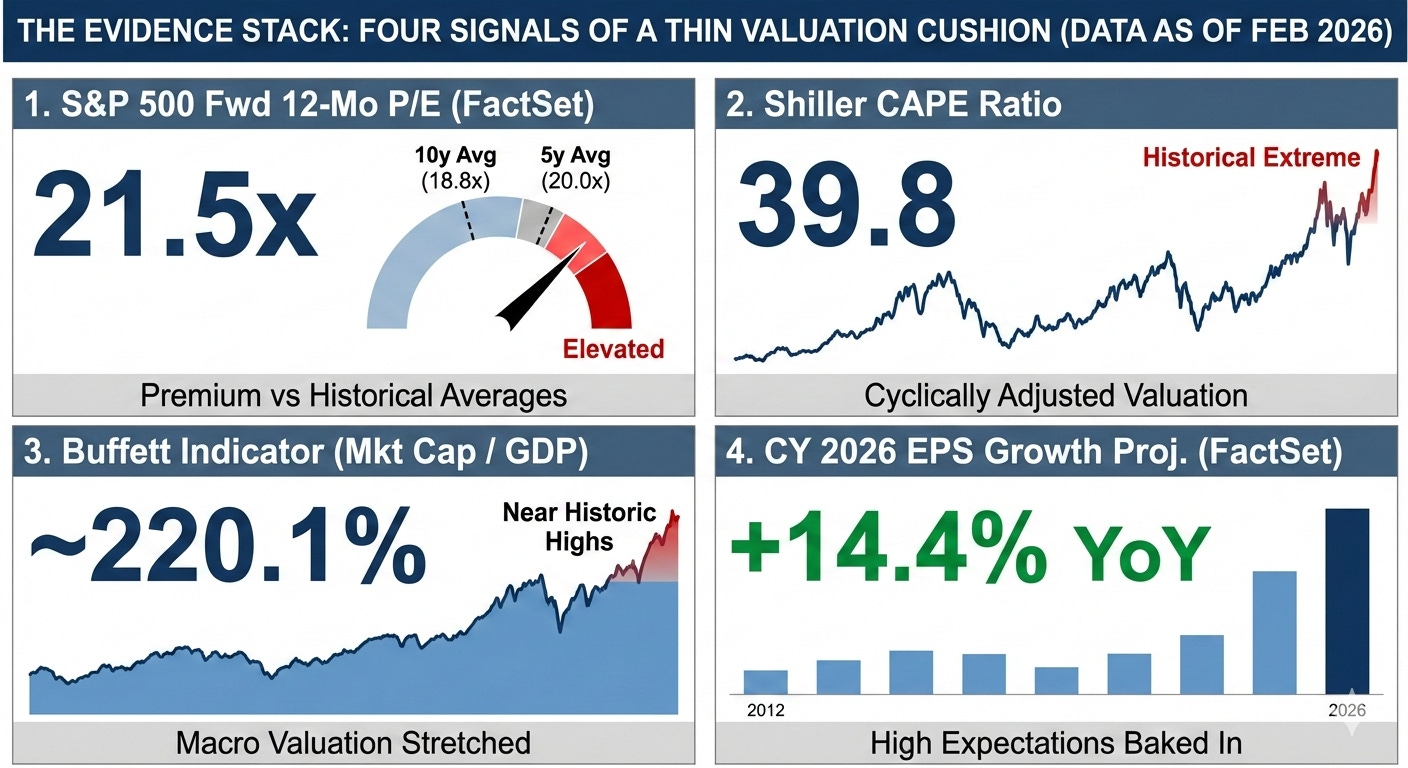

Signal 1 (analyst expectations lens): Forward P/E is elevated, and the earnings-yield gap is thin.

FactSet’s Feb 13, 2026 update puts the S&P 500 forward 12-month P/E at 21.5x, above both the 5-year average (20.0) and 10-year average (18.8).

That implies a forward earnings yield:

E/P ≈ 1 / 21.5 ≈ 4.65%

Versus a 10Y around 4.04%, the simple spread is roughly:

Earnings-yield gap ≈ 0.60%

This is not “true ERP” in the strict sense (earnings yield ≠ expected total equity return). But it is a clean way to express a practical idea: how thin the valuation cushion is versus risk-free yield at current multiples.

Signal 2 (cycle-adjusted lens): CAPE is near historical extremes.

The Shiller CAPE ratio is about 40.2 (25 year highest), which is extremely elevated versus long-run history.

CAPE is not a timing tool, but it is a strong statement about starting valuations over a cycle-adjusted earnings base.

Signal 3 (macro scale lens): Market cap-to-GDP is near extremes.

The “Buffett Indicator” (total market cap / GDP) is around ~220.1% in mid-February 2026, near the upper end of historical experience.

This is a different lens than forward P/E: it’s a macro aggregate valuation versus economic output.

Signal 4 (expectations lens): High EPS growth is already baked in.

FactSet reports analysts project CY 2026 earnings growth of ~14.4% YoY.

When valuation levels are stretched, that growth path stops being “nice to have” and becomes “must deliver.” If the forecast begins to slip via negative revisions (especially in high-weight sectors), the market typically re-prices first via multiples, not via a slow grind in index level.

Mechanism box (keep it explicit and non-overclaimed).

Crude sensitivity (illustrative, not a full model):

If you treat equity like a rough perpetuity (zero growth simplification), then:

required earnings yield ≈

fair P/E ≈

With :

premium 1% → fair P/E ≈ 19.8

premium 2% → fair P/E ≈ 16.6

premium 3% → fair P/E ≈ 14.2

Read-through: at 21.5x forward P/E, the market is effectively tolerating a low required premium and/or assuming durable growth.

More economically intuitive (optional, one line):

Gordon form:

If risk-free rate stays high, either g must hold up (and be broad), or P/E has pressure.

Each signal is measuring something different – analyst forward expectations (Signal 1), cycle-adjusted earnings base (Signal 2), macro aggregate valuation (Signal 3), and embedded growth requirements (Signal 4) – yet all point to the same conclusion: the cushion is thin, and valuation is doing a lot of work.

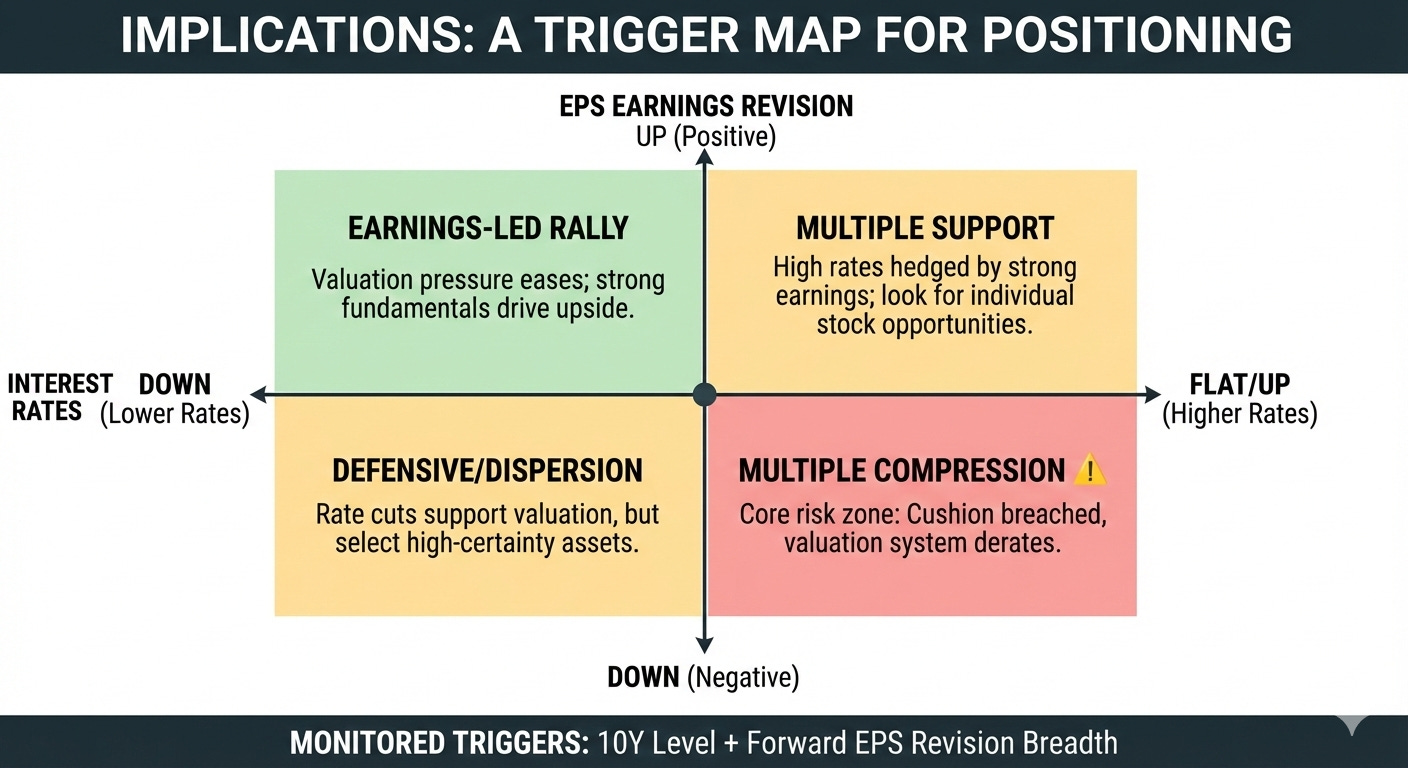

Implications: A Trigger Map for Positioning

Taken together, these measures don’t precisely “time” the market, but they do say something actionable: starting valuation is rich and the cushion is thin – so the next leg is more path-dependent on rates and earnings revisions than on narrative.

With stretched valuations, forward returns skew more earnings-led than multiple-led. The key risk is a specific combination: rates stay ~4% while forward earnings revisions roll over. In that case, the balance of risks shifts toward multiple compression even without a recession.

Triggers you can monitor:

If 10Y remains around ~4% and forward EPS revisions turn broadly negative (FactSet revision trend / breadth),

then multiple compression is more likely to dominate index behavior.If rates fall materially and earnings breadth improves,

then valuation pressure eases; upside can persist, but is still more likely earnings-led than driven by further re-rating.

Portfolio translation (high level, memo style).

Reduce equity duration / multiple risk.

In a high discount-rate regime, the most fragile exposure is “high-duration equity” – premium multiples with cash flows weighted far into the future. This is about what you’re paying, not a blanket “sell growth.”Tilt toward cash-flow certainty and cheaper valuation buckets.

When the cushion is thin, the market tends to reward durable free-cash-flow, balance-sheet resilience, and reasonable multiples – especially when real yields are positive.Prefer defined-risk hedges over heroic timing calls.

Thin cushion regimes produce faster, more nonlinear drawdowns. Defined-risk protection can be a cleaner expression than binary risk-on/risk-off swings.Lean into dispersion and relative value.

Expensive markets often re-price internally: leadership rotation and cross-sectional dispersion can dominate even if the index doesn’t “crash.”

Bottom line: this is not “the market must fall.” It is: the market is priced for a friendly path (some rate relief and continued earnings delivery). If either pillar weakens, the probability-weighted outcome shifts toward multiple compression, and the edge moves from beta to selectivity + structure.