PickAlpha Weekend - Look Into Next Week! | 2026-02-21

1) Weekly Recap • 2) Look Into Next Week | Watchlist: $SPY $DXY $SHY $ZN=F $XLY $NVDA $IGV $IEF $CL=F $XLE $FXE $NG=F $UNG $TLT $FXY $DPZ $HD $LOW •

Weekly Recap

At a glance — Key events

- Claims at 206k vs 225k pushed “higher‑for‑longer” and DXY +0.9% — $DXY, $USDJPY

- EIA crude draw -9.0M bbl to 419.8M drove WTI +5.3% and XLE +1.0% — $CL=F, $XLE

- Treasury 20Y $16.0B auction, BTC 2.36x, high yield 4.664%, nudged 10Y +4 bps — $TLT, $ZN=F

- Supreme Court tariff ruling vs new 10% global surcharge swung trade‑risk premia and broad ETFs — $SPY, $QQQ

U.S. macro this week skewed toward resilient activity and tighter policy expectations. Initial claims at 206k vs 225k and January industrial production at +0.7% m/m reinforced a “no‑landing” narrative, helping push UST 2Y +7 bps and 10Y +4 bps through Thursday, with the 2s10s spread flattening about 3 bps to ~61 bps. Fed Vice Chair Barr’s “on hold for some time” signal and FOMC minutes trimming 2026 cut expectations supported the dollar (DXY +0.9%, USDJPY +1.6%) while pressuring the duration‑sensitive equity complex, even as cyclicals benefited from stronger industrial and housing data.

Cross‑asset price action reflected the mix of firmer growth, higher real rates, inventory‑driven commodities, and shifting trade policy. A -9.0M bbl crude draw to 419.8M lifted WTI +5.3% and XLE +1.0%, feeding inflation‑beta trades against long duration. Treasury’s $16.0B 20Y auction (BTC 2.36x) highlighted ongoing term‑premium sensitivity. Later in the week, the Supreme Court’s invalidation of IEEPA “Liberation Day” tariffs, with potential $130–175B in refunds, briefly supported SPY and QQQ before Trump’s temporary 10% Section 122 global surcharge re‑introduced margin and EM‑exporter risk. Overseas, Japan’s 0.2% annualised Q4 GDP miss and India’s 1.81% WPI kept local policy paths in focus without dominating global risk.

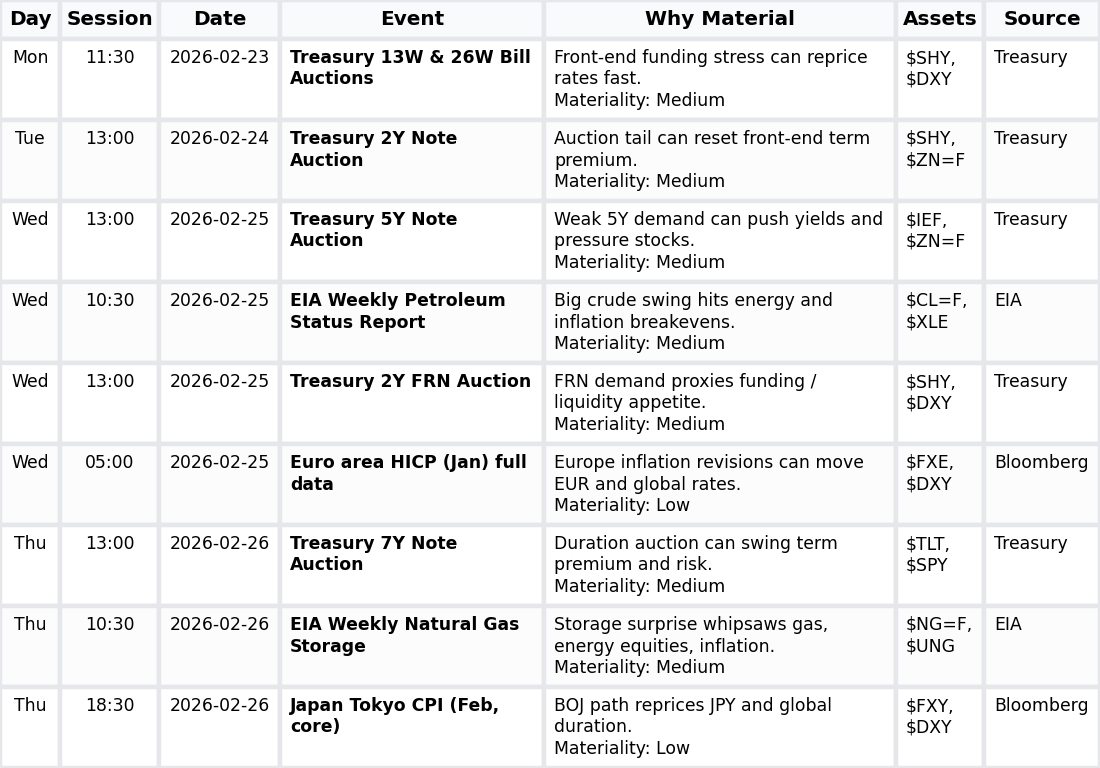

Look Into Next Week

Macro Look

Next week is macro‑light but still rates‑sensitive: Treasury supply from bills through 7Y interacts with recent Fed repricing, while EIA energy data and European/Japanese CPI revisions can nudge inflation expectations, mainly moving U.S. yields, the dollar, energy, and broad risk proxies.

- UST auctions (13W/26W, 2Y, 2Y FRN, 5Y, 7Y; numeric anchor: N/A): supply → yields/term premium → $SHY, $IEF, $TLT.

- U.S. energy inventories (oil, gas; numeric anchor: N/A): inventory swings → WTI/HH → inflation‑beta and $XLE, $UNG.

- Euro area and Tokyo CPI (numeric anchor: N/A): inflation surprises → ECB/BOJ path → EUR/JPY, global duration, $DXY.

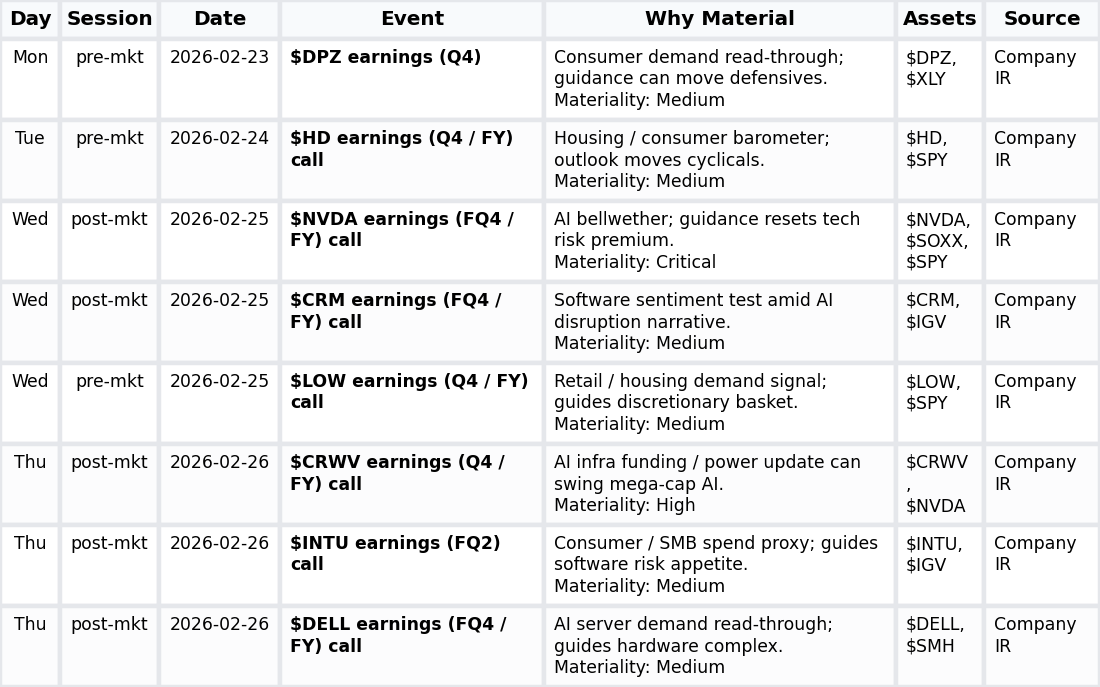

Company Look

Next week is sector‑dispersion heavy: concentrated earnings across AI hardware, cloud/software, and U.S. housing/consumer bellwethers should dominate over pure index‑beta, with guidance on AI capex and household demand steering tech, discretionary, and broader benchmarks.

- U.S. consumer/housing earnings (DPZ, HD, LOW; numeric anchor: N/A): spending and housing tone → guidance revisions → $XLY, $SPY.

- AI/semis and hardware earnings (NVDA, DELL, CRWV; numeric anchor: N/A): AI server demand → capex expectations → $SOXX, $SMH, $SPY.

- Enterprise/software earnings (CRM, INTU; numeric anchor: N/A): SaaS and SMB demand → multiple support/pressure → $IGV, $SPY.

This report is for information only and is not investment advice or a solicitation to buy or sell any security.