PickAlpha Weekend - Look Into Next Week! | 2026-03-21

1) Weekly Recap • 2) Look Into Next Week | Watchlist: $TLT $DXY $SPY $XLY $CL=F $XLI $IWM $FXY $FEZ $TU=F $FXB $XLE $TIP $FV=F $ZN=F $CNM $KBH $XHB •

Weekly Recap

At a glance — Key events

- Fed held 3.50%-3.75%, 2Y +6 bps, S&P -1.36% on decision day — $SPY, $TLT, $DXY

- Brent +8.8% to $112.19 while WTI slipped 0.4% to $98.32 — $CL=F, $BZ=F, $XLE

- Iran waiver frees ~140M bbl over 30 days, pressuring crude benchmarks — $CL=F, $BZ=F, $XOP

- Fed hike odds rose to 25% for 2026, 2Y near 3.89% intraday — $TLT, $IEF, $UUP

Equities de-rated as the Fed’s hold at 3.50%-3.75% and a hawkish SEP left only one 2026 cut, lifting the 2Y by 6 bps to 3.79% and flattening 2s10s to ~46 bps. The S&P 500 fell 1.9%, Nasdaq 2.1%, with AI leadership fading despite Nvidia’s $1T TAM and Micron’s $33.5B FQ3 guide. Higher front-end yields and a 25% priced probability of a 2026 hike tightened financial conditions, weighing on $SPY and $TLT even as DXY finished about 0.9% lower on relatively more hawkish foreign central banks.

An 8.8% Brent surge to $112.19 on Hormuz/Iraq risk initially supported $XLE and breakevens, but the regime flipped late when OFAC’s 30‑day Iran waiver opened a path for roughly 140M stranded barrels, threatening to cap crude benchmarks. EIA’s 6.2M bbl U.S. crude build and 5.4M bbl gasoline draw added nuance to domestic balances. Regulatory flow skewed sector dispersion: proposed U.S. bank capital relief was supportive for $XLF, while DOJ export-indictment headlines hit $SMCI and FDA’s Wegovy HD 7.2 mg approval underpinned obesity-drug optimism in $NVO and $XLV.

(This recap is informational only and not investment advice.)

Look Into Next Week

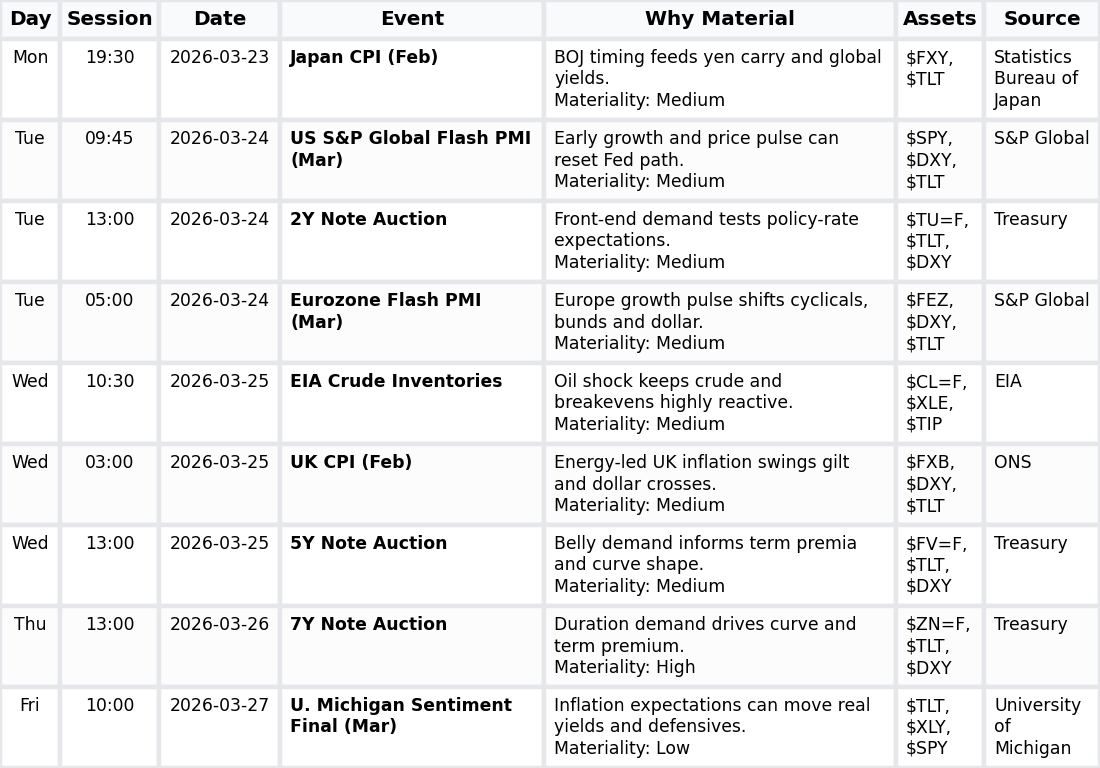

Macro Look

Next week centers on how tighter policy odds and oil volatility transmit through auctions, global growth data, and inflation prints into rates, the dollar, and energy. The heaviest concentration is in U.S. supply and PMIs, with Japan and UK CPI shaping cross-asset reactions to the renewed inflation narrative.

- UST auctions (2Y, 5Y, 7Y; 3 sales, 2–7Y sector) test demand for higher yields. Driver→channel→assets: tail size moves curve and $TLT/$SPY.

- Growth/sentiment data (US/EU PMIs plus U. Michigan; 3 releases) recalibrate activity and price momentum. Driver→channel→assets: composite indices steer $DXY, $TLT, $SPY.

- CPI prints (Japan, UK; 2 reports) refine global inflation and BOJ/BoE paths. Driver→channel→assets: headline/core readings shift $FXY, $FXB, $TLT.

- Oil balances (weekly EIA; Δ_crude_Bbl anchor) intersect with Iran supply shock. Driver→channel→assets: inventory surprise drives $CL=F, $XLE, $TIP.

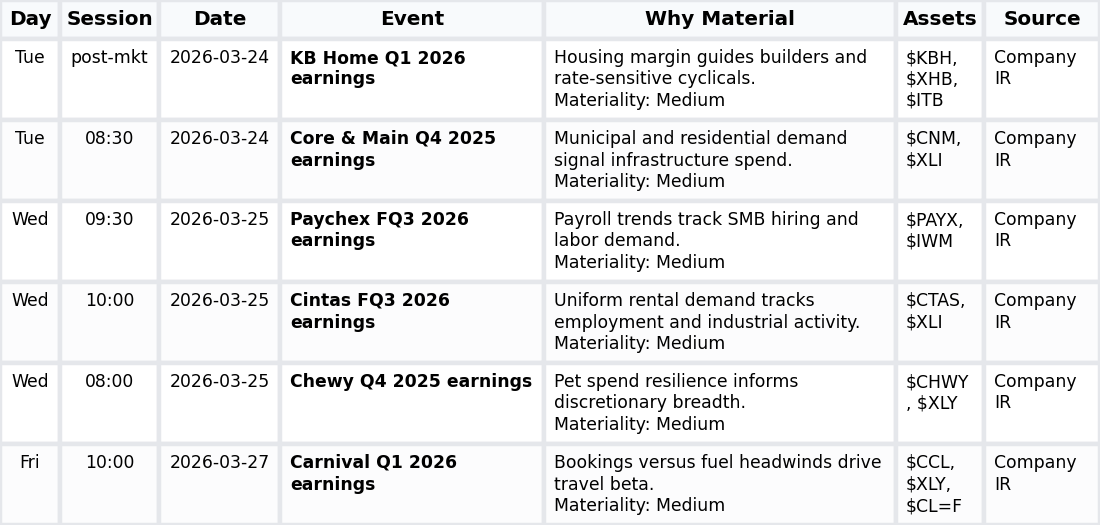

Company Look

Next week is more sector-dispersion than broad index-beta, with a tight cluster of mid-cap earnings spanning housing, infrastructure, industrial services, discretionary, payrolls, and travel. The focus is on how margins and revenues translate tighter financial conditions and oil volatility into demand and pricing across cyclicals.

- Earnings across infrastructure, housing, services, and travel (6 reports: CNM, KBH, CHWY, PAYX, CTAS, CCL) frame demand breadth and margin resilience. Numeric anchor: N/A. Fundamental driver→expectations→sector/index: revenue and margin trends shape outlooks for $XLI, $XLY, $IWM, $SPY.