PickAlpha Weekend - Look Into Next Week! | 2026-03-28

1) Weekly Recap • 2) Look Into Next Week | Watchlist: $SPY $TLT $DXY $IWM $XLI $SOXX $XLP $CL=F $FXI $SHY $IEF $PVH $XRT $RH $XHB $CALM $MSM $LW • What priced this week, and what prices next week

Weekly Recap

At a glance — Key events

• S&P 500 fell 2.1% to 6,368.85 while Nasdaq dropped 3.2%, as mega-cap growth de-rated; $SPY, $QQQ, $XLC.

• Weak $69B 2Y auction at 3.936% with dealers taking 24.1% bear-steepened 2s10s toward ~52–53 bps; $TU, $IEF, $TLT.

• WTI closed at $99.64, +5.4% Friday, with Brent $112.57 on Iran deadline risk, lifting energy; $CL=F, $XLE, $TLT.

Risk assets traded around a combination of supply-driven rate pressure and oil/geopolitical risk. The 2Y yield rose about 3 bps w/w to 3.91% and the 10Y about 5 bps to 4.44%, with quarter-end supply including $69B in 2Ys and $70B in 5Ys weighing on $TU, $IEF and $TLT. Higher yields and a firmer DXY at 100.17 helped push USDJPY up 0.7% to 160.35 and EURUSD down 0.4% to 1.1509, consistent with the week’s modest bear-steepening and risk-off tone.

Oil and inflation signals turned more prominent into week’s end. WTI at $99.64 and Brent at $112.57 came alongside a 6.9M bbl crude inventory build to 456.2M and Iran/Hormuz risk, supporting $XLE and inflation hedges while pressuring long duration. Domestically, import prices rose 1.3% m/m and export prices 1.5% m/m, while Michigan sentiment slipped to 53.3 with 1-year inflation expectations at 3.8%, a mildly stagflationary mix for $SPY, $QQQ and $TLT. Policy and regulatory developments—from dovish BOJ appointments to DOJ subpoenas in a $110B media deal—added idiosyncratic cross-asset noise.

Look Into Next Week

Macro Look

Next week’s macro tape is labor- and activity-heavy, with U.S. payrolls, ISM surveys and claims likely to dominate. These prints, alongside China’s PMI and EIA inventories, mainly reprice rates and the USD, with secondary effects on cyclicals, energy and broad risk proxies.

• Labor-market data (ADP, JOLTS, NFP; NFP score 92) → jobs strength/weakness→Fed path→$TLT/$SPY/$DXY. Numeric anchor: 92.

• ISM manufacturing/services (scores 81, 78) → activity/prices→rate expectations→cyclicals and duration; driver→rates→$SPY/$TLT/$SOXX. Numeric anchor: 81.

• China NBS manufacturing PMI (score 74) → China growth pulse→commodities/chips→global beta $FXI/$SOXX/$SPY. Numeric anchor: 74.

• EIA crude inventories (score 84) → stock changes→oil prices→inflation/rates $CL=F/$XLE/$TLT. Numeric anchor: 84.

• Weekly jobless claims (score 72) → layoffs→recession odds→curve/risk $TLT/$SPY/$IWM. Numeric anchor: 72.

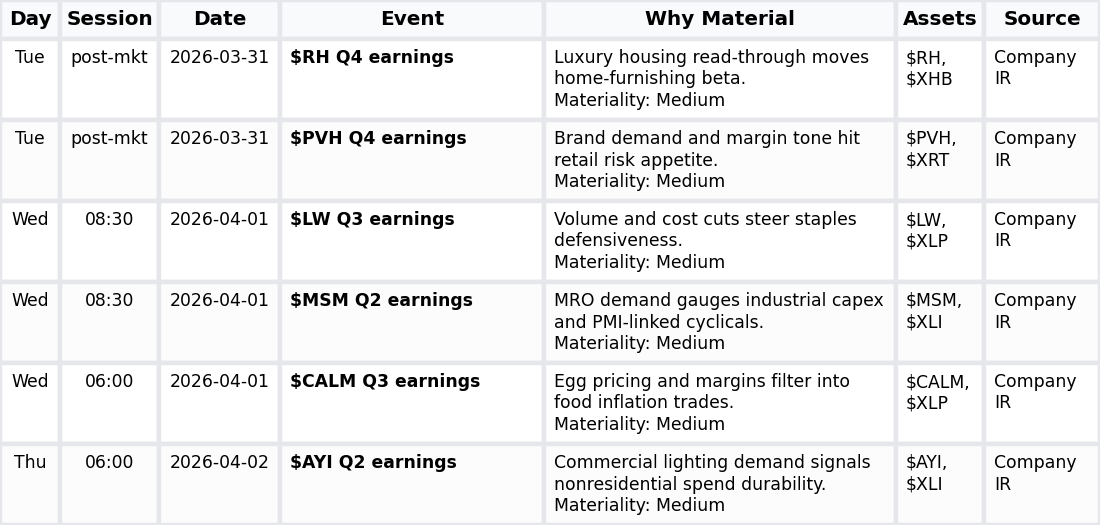

Company Look

Next week is skewed toward sector dispersion rather than broad index beta, with a cluster of mid-cap earnings across discretionary, staples and industrials. The main themes are U.S. consumer resilience, housing-adjacent demand and industrial capex, with read-throughs to $XRT, $XLP, $XLI and, by extension, $SPY.

• Discretionary/retail earnings ($PVH, $RH) → holiday/luxury demand→consumer-spend expectations→$PVH/$RH/$XRT/$XHB/$SPY. Numeric anchor: N/A.

• Staples/food earnings ($CALM, $LW) → input costs and pricing power→defensiveness versus inflation→$CALM/$LW/$XLP/$SPY. Numeric anchor: N/A.

• Industrial/capex earnings ($MSM, $AYI) → factory and nonresidential spend→cycle durability→$MSM/$AYI/$XLI/$SPY. Numeric anchor: N/A.

This note is for informational purposes only and is not investment advice or a solicitation to buy or sell any security.