PickAlpha Weekend - Look Into Next Week! | 2026-03-07

1) Weekly Recap • 2) Look Into Next Week | Watchlist: $SPY $TLT $DXY $XLK $QQQ $TSLA $HPE $NIO $KWEB $SHY $ORCL $CPB $XLP $CL=F $XLE $IEF $LI $DG •

Weekly Recap

At a glance — Key events

- WTI jumped 35.6% to $90.90, lifting $XLE and pressuring $TLT as inflation beta repriced.

- U.S. payrolls fell 92k, unemployment hit 4.4%, jolting $SPY, $TLT, $UUP into stagflation debate.

- Q4 nonfarm productivity beat at 2.8% vs ~1.8% consensus, modestly supporting $SPY, $QQQ, $TLT.

- 10Y yield rose 17 bps to 4.142% while DXY gained 1.4%, weighing on $SPX, $IWM.

Oil and labor were the dominant macro drivers. An effective Hormuz closure delayed roughly 140M barrels and sent WTI up 35.6% and Brent 27.9%, boosting $XLE but pressuring long duration as the 10Y climbed 17 bps to 4.142%. That shock overrode EIA’s 3.5M‑barrel inventory build and helped push the VIX to a 29.5 close. On data, February payrolls printed -92k versus +59k consensus with unemployment at 4.4% and wages up 0.4% MoM, while ISM Services held at 56.1 and jobless claims stayed low at 213k, leaving a stagflation‑flavored mix.

Cross‑asset pricing reflected that tension. The S&P 500 fell 2.0%, Nasdaq 1.2%, and Russell 2000 4.1%, with Energy up 1.2% in $XLE and Health Care down 4.7% in $XLV. Warsh’s Fed Chair nomination kept a hawkish bias in focus alongside a $125B refunding that cleared but did not cap term premia. AI remained a counterweight: Broadcom delivered $19.31B revenue, $8.4B AI revenue, and a $22.0B Q2 guide, while Marvell outlined a ~$15B FY2028 target versus $12.92B consensus, supporting $SOXX and partially cushioning broader cyclical weakness.

Look Into Next Week

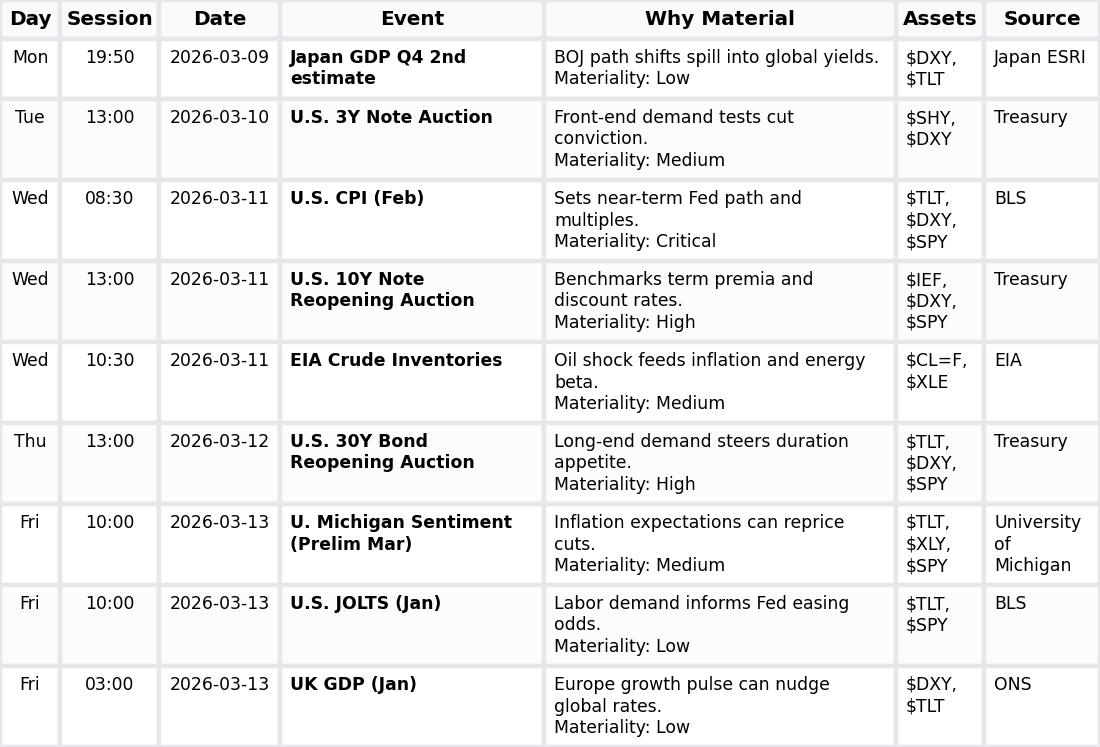

Macro Look

Next week centers on U.S. inflation, oil, and Treasury supply. February CPI and the oil‑linked EIA report will test whether the recent 35.6% WTI spike sticks in inflation expectations, while 3Y/10Y/30Y auctions and global growth prints (Japan, UK) feed back into rates, the dollar, and overall risk appetite.

- Inflation prints (CPI, materiality 93) anchor the week; core MoM surprises steer inflation→rates→USD/equity duration for $TLT, $DXY, $SPY.

- UST auctions (3Y/10Y/30Y, combined materiality 249) test auction demand→yields→discount rates for $SHY, $IEF, $SPY.

- Oil/inventories (EIA, materiality 76) channel Δ_crude_Bbl→WTI→breakevens/energy beta for $CL=F, $XLE, $SPY.

- Global/US growth and sentiment (OTHER, total materiality 259) drive GDP/sentiment→central banks→USTs/FX for $DXY, $TLT, $SPY.

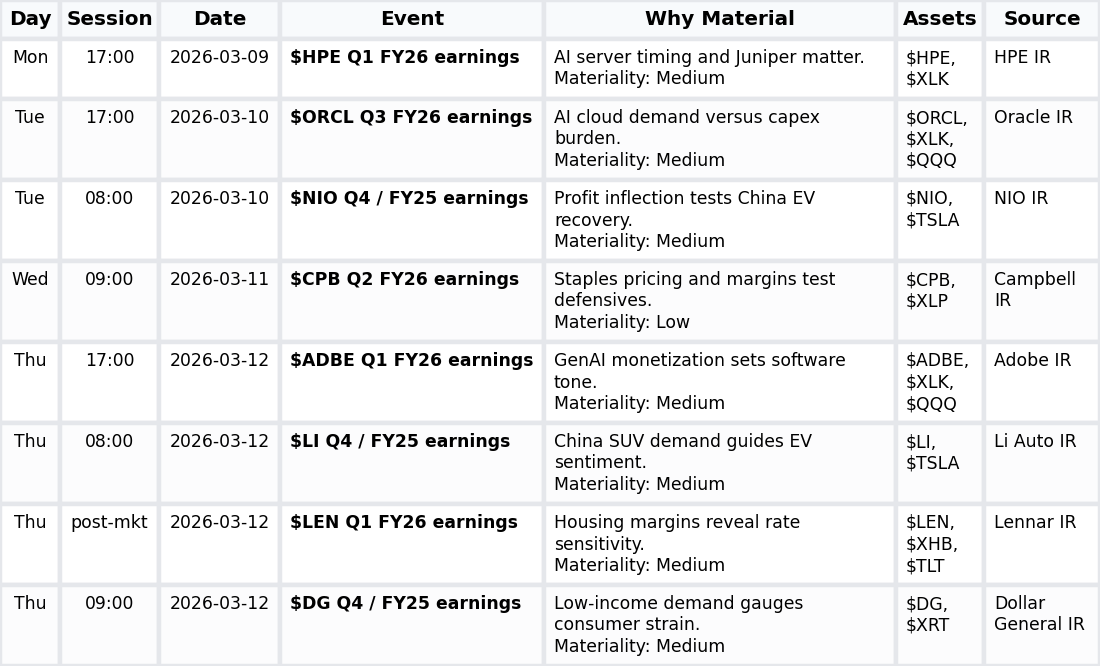

Company Look

Next week is skewed to sector dispersion rather than pure index beta, with a heavy earnings slate across AI infrastructure/software, China EVs, U.S. staples, value retail, and housing. Tech prints from $ORCL, $ADBE, and $HPE frame AI capex and monetization, while $NIO, $LI, $DG, $CPB, and $LEN update views on consumer health and rate sensitivity.

- Earnings (aggregate materiality high; numeric anchor: N/A) drive revenue/margins→guidance versus AI/consumer expectations→sector/index dispersion across $HPE, $ORCL, $ADBE, $NIO, $LI, $DG, $CPB, $LEN, XLK 0.00%↑ $XRT.