Should You Leave Your Portfolio Alone During the World Cup?

A behavioral-finance look at why football, sleep, sentiment, and 104 matches may matter at the edges of the market.

The Old Anomaly: World Cup Windows Have Looked Weak for U.S. Stocks

The clean answer is simple.

You should not sell your portfolio just because the World Cup starts.

But history is not completely silent.

In a 2010 paper published in the Journal of Financial and Quantitative Analysis, Guy Kaplanski and Haim Levy studied what they called the “FIFA World Cup effect” on the U.S. stock market. Their paper, Exploitable Predictable Irrationality: The FIFA World Cup Effect on the U.S. Stock Market, found that the average U.S. market return during the World Cup “effect period” was -2.58%, compared with +1.21% for all-day average returns over the same period length.

Academic research has linked World Cup windows, soccer losses, and national-team matches to investor sentiment, abnormal returns, and lower trading activity.

That sounds dramatic.

But it should not be read as a simple trading rule.

The study is important because it points to a behavioral anomaly. It does not prove that every future World Cup will hurt stocks. Markets change. Trading is more automated. Information moves faster. The investor base is different.

So the better takeaway is not:

“World Cup = sell stocks.”

The better takeaway is:

“Major global events can pull attention away from markets, and that can show up in returns.”

For long-term investors, the World Cup is not a reason to abandon a portfolio.

For market observers, it is a useful reminder: even liquid markets are still priced by distracted humans.

The Real Mechanism: Mood, Loss Aversion, and Investor Attention

The World Cup does not change Apple’s earnings.

It does not change Nvidia’s data center demand.

It does not change the Fed’s reaction function.

What it can change is mood.

In Sports Sentiment and Stock Returns, published in the Journal of Finance in 2007, Alex Edmans, Diego García, and Øyvind Norli used international soccer results as a proxy for investor mood. They found that a loss in the World Cup elimination stage was followed by a next-day abnormal stock return of about -49 basis points in the losing country’s market. The effect was stronger in small stocks and in more important games.

That is classic loss aversion.

Wins help mood.

Losses hurt more.

There is also an attention channel.

Michael Ehrmann and David-Jan Jansen studied stock market trading in 15 countries during the 2010 and 2014 FIFA World Cups. In their 2017 Journal of Money, Credit and Banking paper, The Pitch Rather Than the Pit, they found that traded volumes declined by as much as 48% when the national team was playing. Local markets could also temporarily decouple from global market moves.

A later 2023 Global Finance Journal paper by Jinghan Cai, Manyi Fan, and Chiu Yu Ko separated two channels: sleeplessness and distraction. They found market daily returns of about -26 bps around sleep loss and -22 bps around trading-hour distraction.

The market may be efficient.

The people watching it are not always awake.

Why 2026 Is Different: North America Turns the World Cup Into a Consumption Event

2026 is not just another World Cup.

It is the first 48-team World Cup.

It has 104 matches.

It will be played across 16 host cities in the United States, Canada, and Mexico.

That matters because the 2026 tournament is not only a sports event. It is also a travel, lodging, food, media, and advertising event.

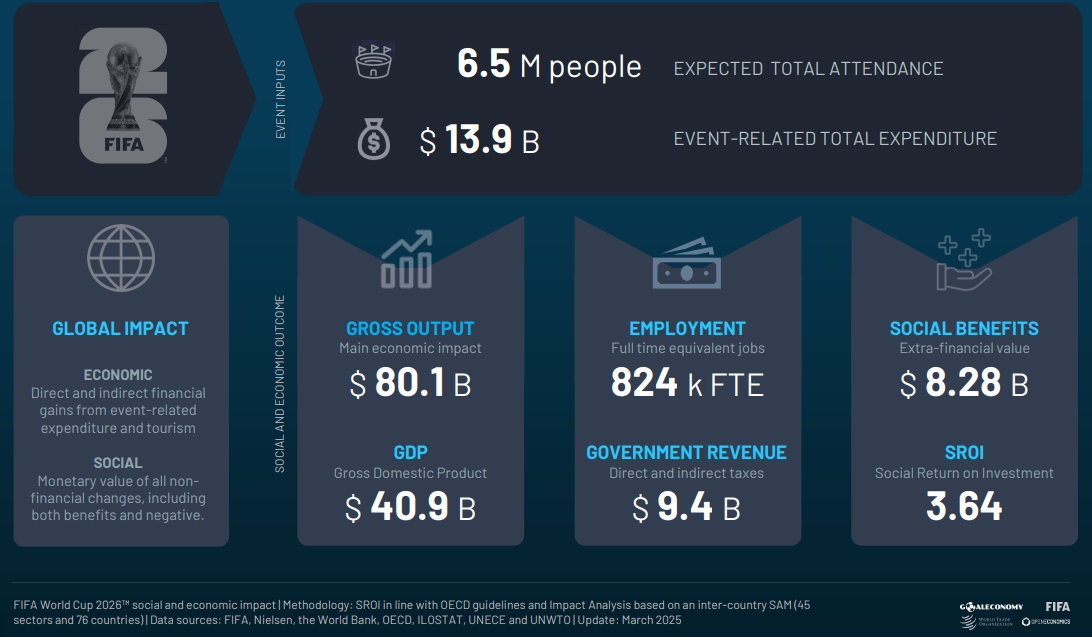

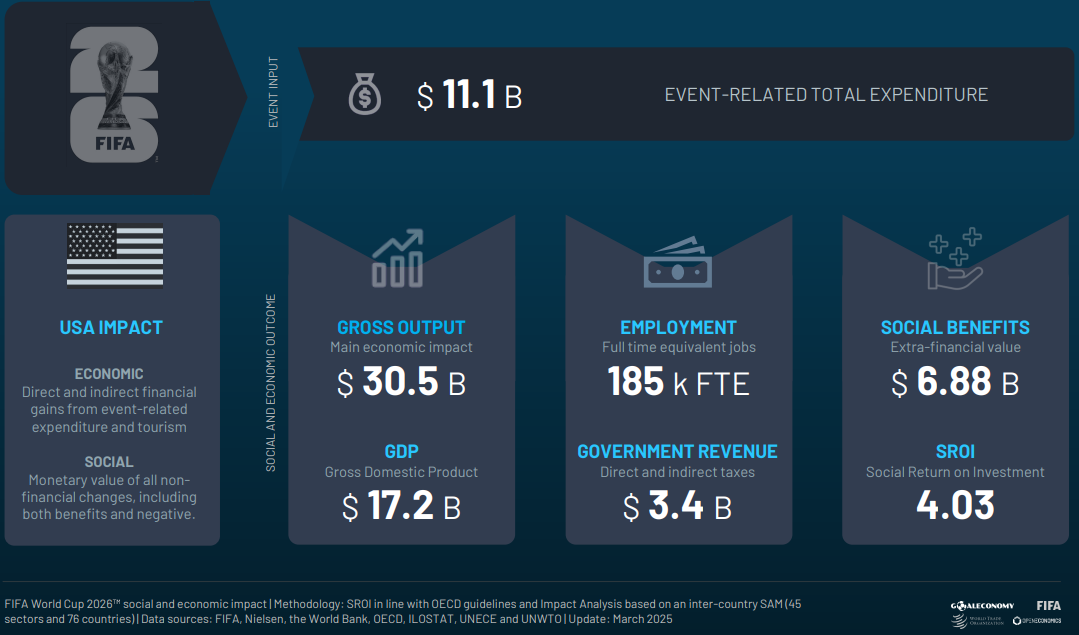

FIFA and the World Trade Organization released a 2025 socioeconomic impact study prepared by OpenEconomics. The study estimated that 6.5 million people could attend the tournament across the host countries. It also estimated up to $40.9 billion in global GDP impact and nearly 824,000 full-time-equivalent jobs globally.

2026 is less a macro GDP story and more a localized spending event across travel, lodging, food, media, and advertising.

Those are large numbers.

But they should not be confused with a broad U.S. macro boom.

Saxo’s May 2026 analysis made the right distinction. The World Cup can matter locally, but even optimistic estimates put the U.S. GDP impact at less than 0.1% of national output.

That is the key.

This is not a reason to change your whole market view.

It is a reason to look for concentrated revenue pockets.

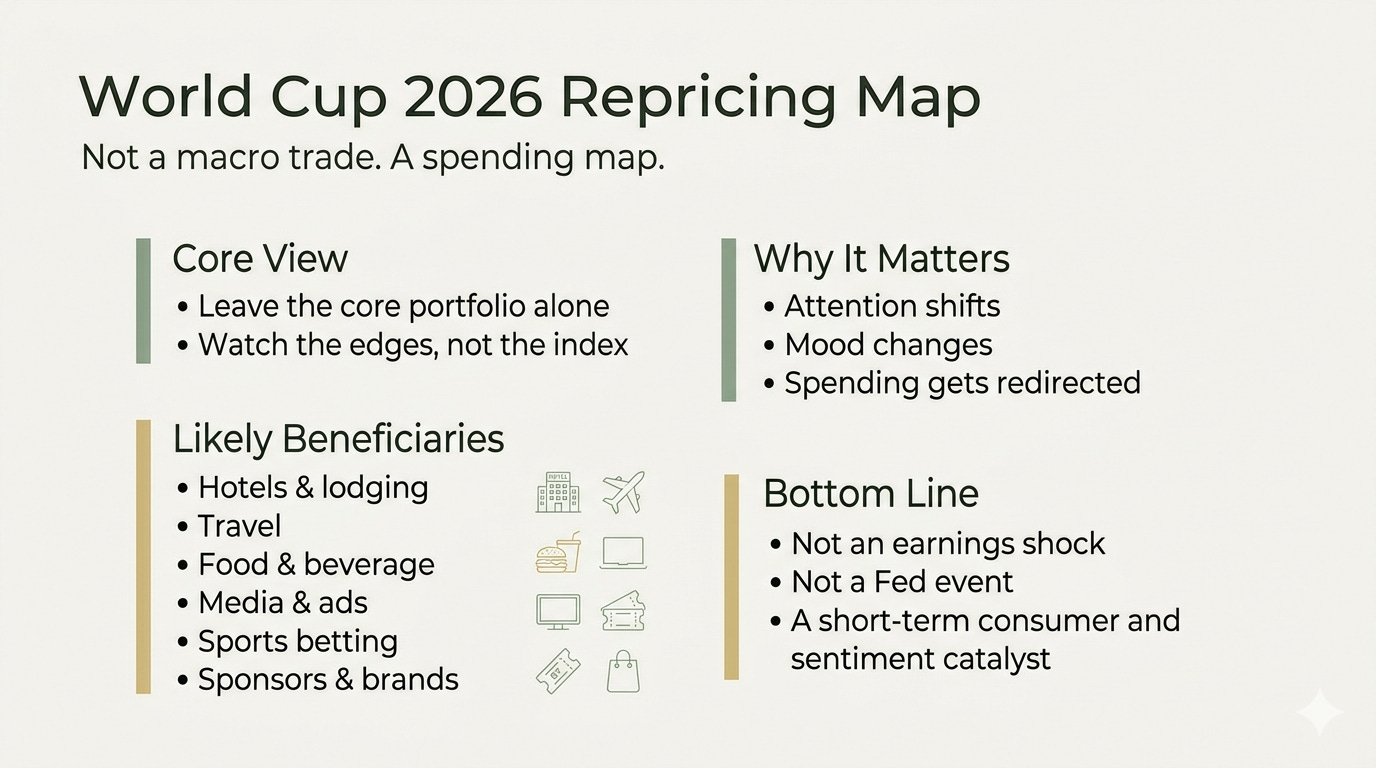

The Repricing Map: What Actually Matters

The lazy trade is to ask whether the S&P 500 goes up or down during the World Cup.

The better question is simpler:

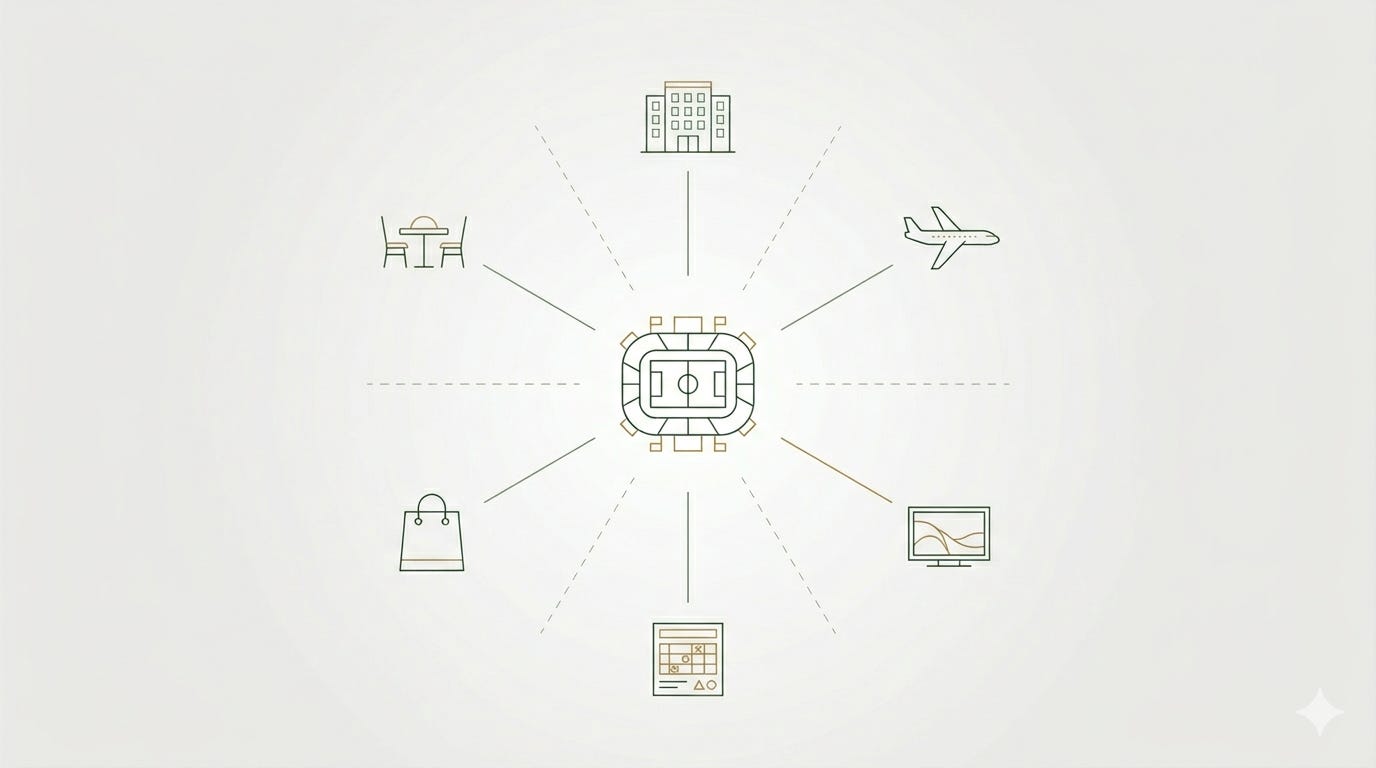

Where does the spending go?

The most direct buckets are lodging, travel, food, beverages, media, advertising, sports betting, and sponsor exposure.

Reuters reported on June 5, 2026, that brokerages expect the tournament to benefit sectors from tourism to retail and athletic wear. Analysts cited hotel operators, online travel platforms, airlines, beer companies, retailers, sportswear brands, restaurants, delivery names, media platforms, and betting operators.

Deutsche Bank analysts made a similar point. According to Business Insider’s June 2026 report, Deutsche highlighted lodging, transportation, food and beverage, media, tech, and gaming as the cleaner World Cup exposure areas. The logic is not complicated. More matches mean more travel. More travel means more rooms, meals, drinks, ads, and bets.

There is also a sponsor angle.

IG’s May 2026 analysis found that a basket of major World Cup sponsors returned an average of 7.1% during recent tournament windows, versus 1.9% for the S&P 500.

Interesting.

But not automatic.

This is a catalyst map, not a magic alpha machine.

The Portfolio Answer: Leave the Core Alone, Watch the Edges

So should you leave your portfolio intact during the World Cup?

For a diversified long-term portfolio, yes.

The World Cup is not a reason to sell core holdings.

It is not a recession signal.

It is not an earnings shock.

It is not a Fed event.

The strongest evidence says something more subtle. The World Cup can affect mood, attention, sleep, trading volume, and short-term risk appetite. That can matter at the margin. It does not mean investors should rebuild their portfolios around match schedules.

The better playbook is simple.

Leave the core alone.

Watch the edges.

If there is a market effect, it is more likely to show up through sentiment and attention than through fundamentals. If there is an earnings effect, it is more likely to show up in specific revenue channels: hotels, travel, beer, restaurants, media, betting, retail, and sponsors.

That is the honest answer.

The biggest risk to your portfolio during the World Cup is probably not football.

It is using football as an excuse to overtrade.

Go deeper

For latest developments, check our daily Morning Report.

For intraday developments, follow our Midday posts.

For the close, the wrap, and next-day trade ideas, read the Evening Memo.

For deeper single-name work, read Forward Valuation.

For longer thematic research, read Deep Dive.

Informational only; not investment advice. Sources deemed reliable.