The New Rule for Software Stocks: Show Me AI Revenue

The software market is developing a new AI monetization filter.

The AI trade may be entering its second phase.

Phase one rewarded the companies building the infrastructure: chips, servers, memory, networking, and power.

Phase two may reward the software companies that can prove one thing Wall Street now cares about: AI is not just a feature – it is revenue.

For most of the past year, software has traded like one of AI’s first victims. The bear case was simple. If AI reduces the need for traditional knowledge workers, then seat-based SaaS revenue could come under pressure. If AI agents can directly complete more workflows, then some software applications may lose pricing power. That narrative hit the sector hard, and many former market favorites suffered deep drawdowns.

But the latest earnings season has complicated that story. AI is not destroying software evenly. It is separating the companies that can turn AI into measurable revenue from the companies that can only attach AI branding to existing products.

That distinction now matters more than ever.

This edition is free for all readers. Future Forward Valuation pieces will generally be part of PickAlpha Pro, where we publish deeper thematic research, ticker maps, and forward-looking valuation frameworks.

Earnings season showed a split, not a collapse

The most important takeaway from this software earnings season is not that all software is back. It is that the market is becoming much more selective.

Several software companies delivered sharp post-earnings rallies. Snowflake (SNOW), Datadog (DDOG), Atlassian (TEAM), Twilio (TWLO), and Figma all saw strong reactions after reporting results. Cybersecurity names such as CrowdStrike (CRWD), Palo Alto Networks (PANW), and Fortinet (FTNT) also staged major rebounds or strong post-earnings moves.

At first glance, these companies do not look closely related. SNOW is a data cloud and analytics platform. DDOG provides observability and monitoring for modern IT systems. TEAM owns collaboration and software-development tools such as Jira and Confluence. TWLO provides communications APIs for voice, text, and messaging. Figma is a collaborative design platform. CRWD, PANW, and FTNT sit in cybersecurity.

Different end markets. Different products. Different revenue mixes.

But the market reaction suggests a common thread: these are software companies where AI can plausibly increase usage, deepen enterprise adoption, or create a new monetization layer.

That is the key filter. The market is no longer rewarding companies simply for saying they have AI. It is rewarding companies that can show AI in the revenue line.

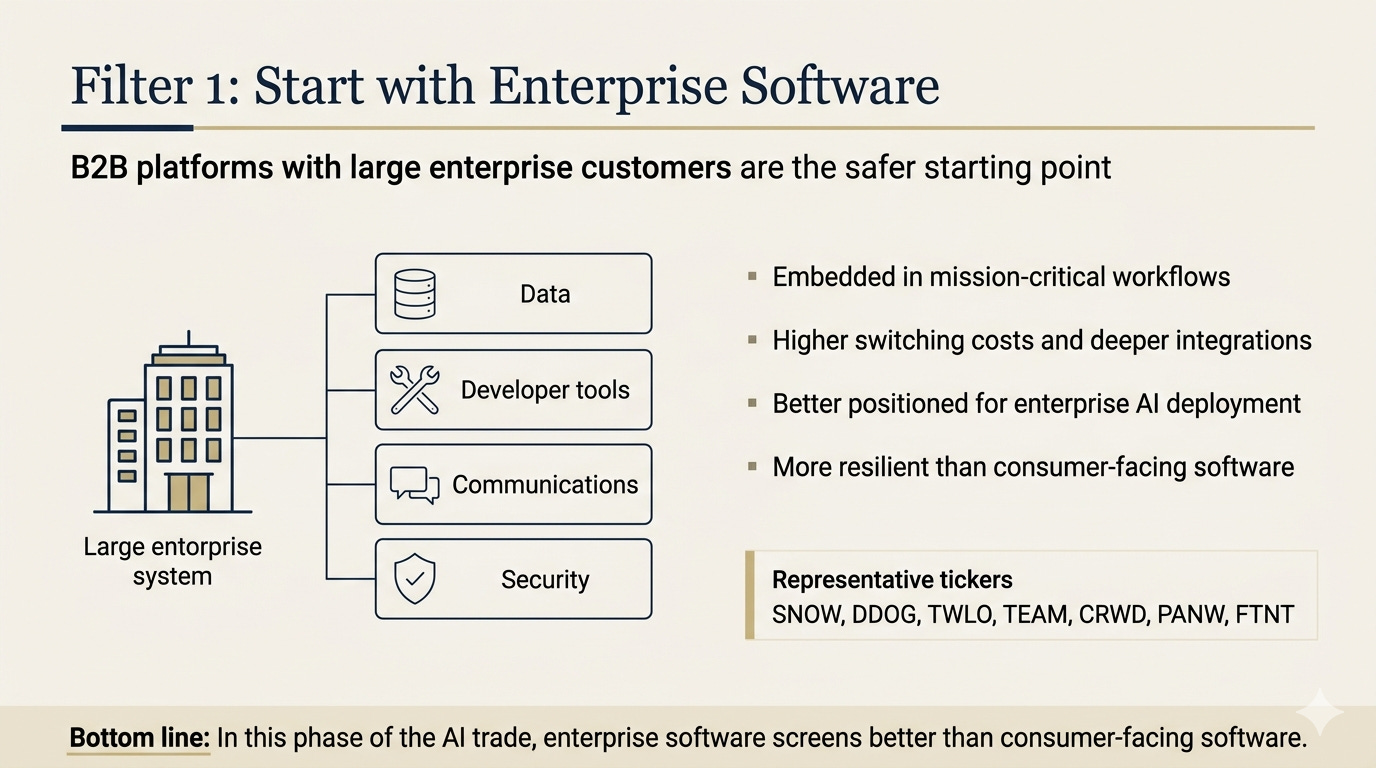

The first filter: enterprise software beats consumer-facing software

The first filter is customer base. The software companies being rewarded are mostly B2B companies, and in many cases they serve large enterprises.

That matters because enterprise software is harder to replace. These products are embedded into data pipelines, developer workflows, IT operations, security architecture, and customer communication systems. Large companies do not casually rip out core infrastructure, especially when those systems touch compliance, uptime, data security, or mission-critical workflows.

This is why SNOW, DDOG, TEAM, TWLO, CRWD, PANW, and FTNT screen better than more consumer-facing or small-business-oriented software names. They are not just selling convenience. They are selling infrastructure, workflow control, security, or system reliability.

SNOW benefits from the enterprise need to organize, query, and govern data. If companies want to run AI on internal data, the data layer becomes more important, not less. DDOG benefits from the increasing complexity of cloud infrastructure, AI workloads, GPU monitoring, and distributed systems. TWLO benefits if more customer interactions move toward automated voice, messaging, and AI-driven service workflows. CRWD and PANW benefit from the reality that more AI agents, more automated code, and more machine-driven workflows can expand the attack surface.

This does not mean every enterprise software stock is safe. It means the starting point is better. Enterprise platforms have stronger switching costs, larger customers, deeper integrations, and more ways to monetize AI through usage expansion.

By contrast, software with more consumer exposure, simpler workflows, or lower switching costs may face more direct pressure. If the product can be replicated by an AI agent, or if the customer is highly price-sensitive, the AI risk is harder to dismiss.

That is the first screen: in this phase of the AI trade, investors should start with enterprise software before moving down the stack into weaker, more discretionary applications.

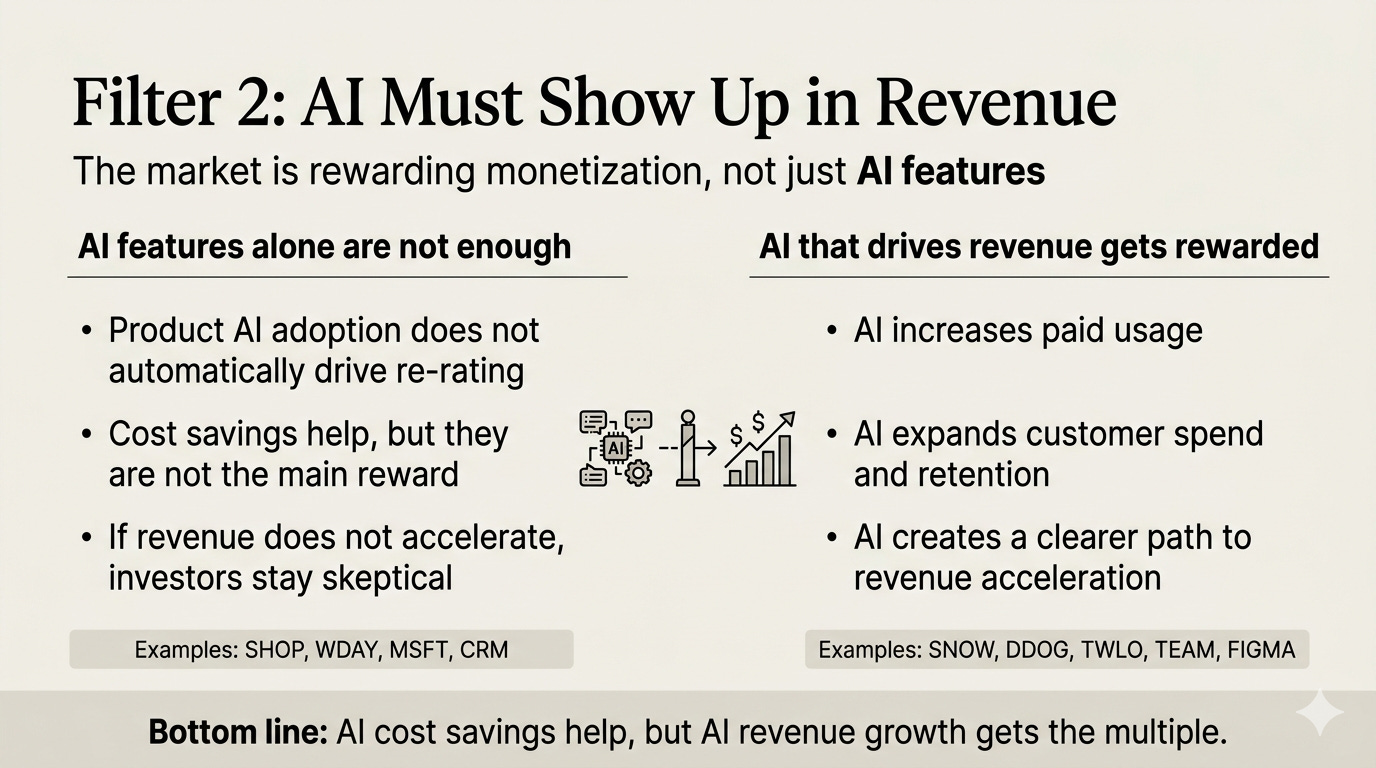

The second filter: AI must show up in revenue

The second filter is the most important one: AI must show up in revenue.

This is where the market has become much stricter. Investors do not want to hear that a company has added AI features. Every software company now has AI features. The question is whether AI is expanding revenue growth, customer spend, net revenue retention, or paid usage.

SNOW is one of the clearest examples. The company’s growth accelerated, and management pointed to AI products such as Cortex and Snowflake Intelligence as contributors. The logic is simple: if AI increases the need to access, structure, analyze, and govern enterprise data, SNOW can capture more consumption. AI is not just a product label. It can become a driver of data usage.

DDOG tells a similar story from the observability side. AI workloads create monitoring problems. Companies running AI applications need to track servers, logs, cloud infrastructure, networks, GPU usage, model performance, and system reliability. If AI increases infrastructure complexity, DDOG’s monitoring layer becomes more valuable. That is why AI-native customers and GPU monitoring matter for the DDOG thesis.

TWLO is another example. Voice AI and AI-powered customer service can increase demand for communication APIs. If companies deploy more automated agents for customer calls, texts, verification, and support workflows, TWLO can see more usage across its platform. The key is not that TWLO has an AI story. The key is that AI can create more communication volume.

TEAM and Figma are more nuanced but still important. They were historically more seat-based, but both are trying to turn AI into an incremental paid layer. TEAM’s Rovo gives Atlassian a usage-linked AI assistant inside existing enterprise workflows. Figma’s AI features may expand design from a specialized function into a broader product workflow used by more teams. In both cases, the bull case depends on AI increasing paid usage and customer expansion, not simply improving the product demo.

This is why the market has been less forgiving toward companies where AI adoption does not clearly translate into revenue acceleration.

Shopify (SHOP) may be one of the strongest AI adopters in software from a product perspective. It has integrated AI across many merchant workflows. But if that does not clearly accelerate revenue growth, investors may still treat the stock harshly. Workday (WDAY) is another useful contrast. AI-driven efficiency and better margins are helpful, but if revenue growth remains ordinary, the market may not reward the stock.

That is the new rule for software: AI cost savings help, but AI revenue growth gets the multiple.

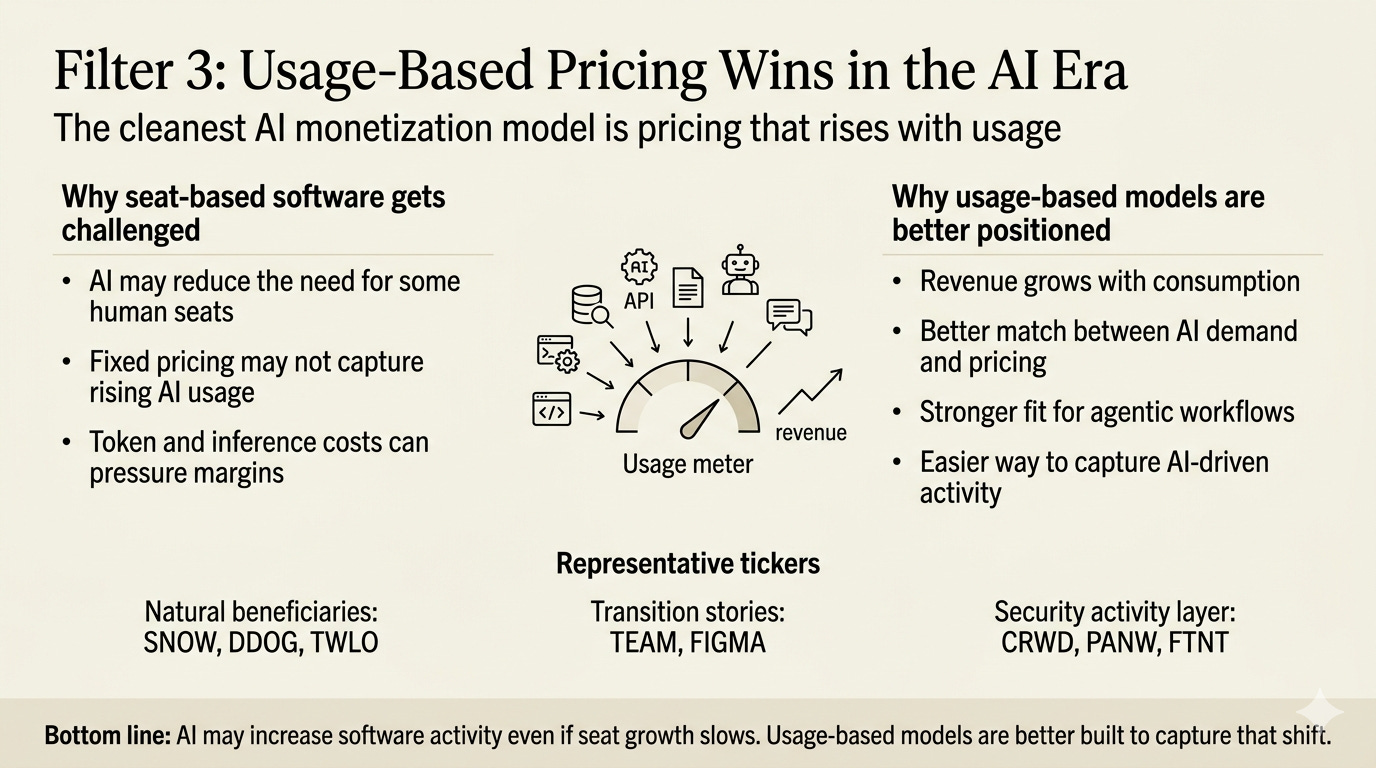

The third filter: usage-based pricing is becoming the cleanest AI model

The third filter is business model. In the AI era, usage-based pricing is becoming the cleanest way for software companies to capture AI-driven demand.

Traditional SaaS was built around seats. A company paid for a fixed number of users. That model worked extremely well for decades because software had very high gross margins. Adding one more user usually created very little incremental cost.

AI changes that equation. When users consume AI features, the software provider may face real inference costs. Tokens are not free. If usage rises but pricing remains fixed, the vendor may absorb more cost without capturing enough revenue upside.

That is why usage-based models matter.

SNOW, DDOG, and TWLO are the cleanest examples in this group. Their businesses already have strong usage-based or consumption-linked elements. SNOW is tied to data consumption and analytics workloads. DDOG is tied to infrastructure monitoring, logs, usage, and observability demand. TWLO is tied to API calls, messages, voice, and communication volumes.

If AI increases the number of queries, logs, calls, messages, workflows, or automated tasks, these companies have a more natural way to monetize that activity.

TEAM and Figma show the second path: seat-based companies trying to add usage-linked AI modules. That transition is important because it gives them a way to monetize AI beyond simply charging for more human users. If AI reduces the need for some seats but increases total workflow activity, the companies that charge only by seat may struggle. The companies that can charge by usage, credits, consumption, or AI activity have a better chance of capturing the upside.

This is also why infrastructure-like software may be the most attractive part of the application layer right now.

SNOW, DDOG, and TWLO are not pure application software in the traditional sense. They sit close to the activity layer of the enterprise technology stack. SNOW sits near the data layer. DDOG sits near the monitoring and infrastructure layer. TWLO sits near the communications layer. CRWD, PANW, and FTNT sit near the security layer.

That positioning matters because AI agents should increase machine-driven activity. More agents means more data access, more API calls, more logs, more cloud workloads, more security events, and more monitoring needs. The more software activity AI creates, the more these infrastructure-like software companies can benefit.

Cybersecurity deserves special attention here. CRWD, PANW, and FTNT are not the same kind of usage-based stories as SNOW or DDOG, but the demand logic is powerful. More AI-generated code, more automated agents, and more machine-to-machine interactions can create new vulnerabilities. That expands the need for endpoint security, network security, cloud security, identity protection, and threat detection.

The risk is timing. Security demand may be structurally stronger, but revenue recognition can lag the narrative. That is why cybersecurity should be treated as a strong thematic beneficiary, but not automatically the cleanest near-term earnings acceleration trade.

The bigger caution is for old software companies trying to reinvent themselves with AI copilots.

Microsoft (MSFT), Salesforce (CRM), Shopify (SHOP), Workday (WDAY), and many other software incumbents have all pushed AI features aggressively. But the market is learning to ask a harder question: are these products changing revenue growth, or are they simply defending the existing base?

That distinction matters because AI features themselves may become commoditized. Foundation models are improving quickly. A software company’s in-house AI assistant can look useful one quarter and outdated the next. The durable advantage may not come from having the best model. It may come from workflow ownership, distribution, data access, enterprise trust, compliance, security, and pricing power.

Conclusion

Our view is that the software opportunity is real, but the screen has changed.

The best AI software candidates are not necessarily the companies with the loudest AI message. They are the companies where AI increases measurable usage, where usage converts into revenue, and where the business model can absorb token costs without margin damage.

For now, that points investors toward enterprise software, AI revenue acceleration, and usage-based or infrastructure-like models.

The market is no longer asking whether a software company has AI.

It is asking whether AI can change the revenue line.

That is the new AI monetization filter.

Go deeper -

For intraday developments, follow our Midday posts.

For the close, the wrap, and next-day trade ideas, read the Evening Memo.

For deeper work, Forward Valuation covers multi-week single-name setups.

Deep Dive is where we publish full thematic research.

Informational only; not investment advice. Sources deemed reliable.

Excellent breakdown!